|

Slide 14

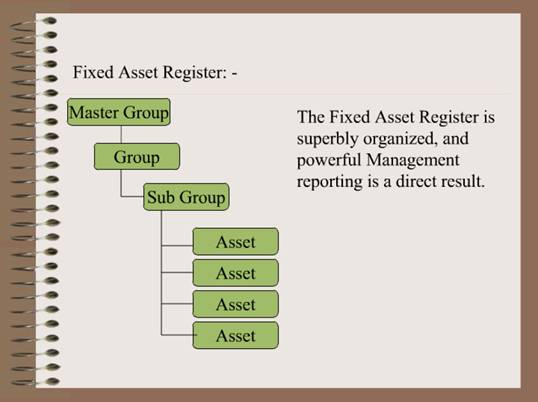

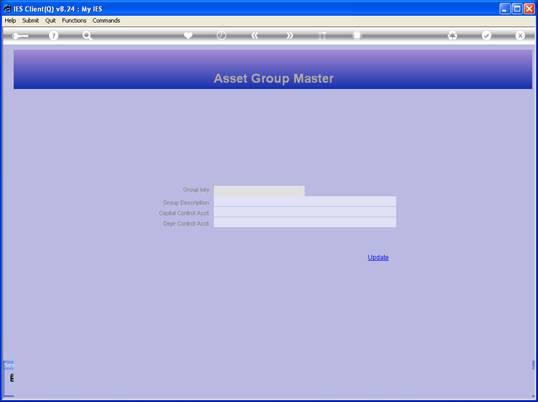

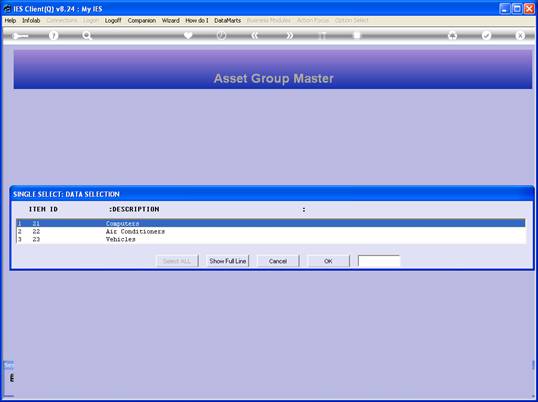

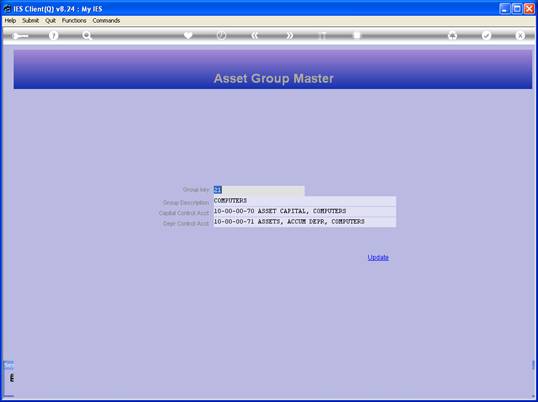

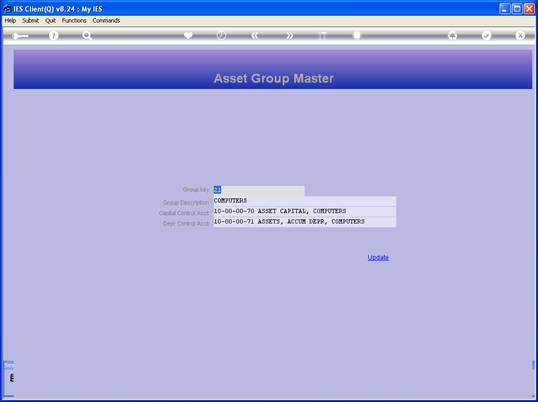

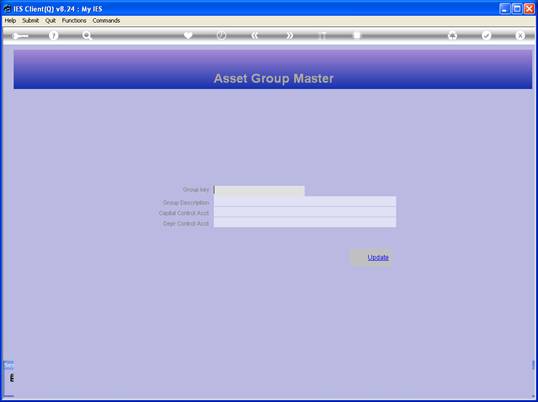

Slide notes: Each Group has a Group Code, a

Name, and of course has a specified Control Account for each of Capital and

Accumulated Depreciation. Once a Group has been created, we can only change

its Name afterwards, but not the Control Accounts. Every Asset Master is

linked to some Group, and can be moved by being re-classified. But the

Control Accounts for a Group cannot

be changed.

|