|

Slide 1

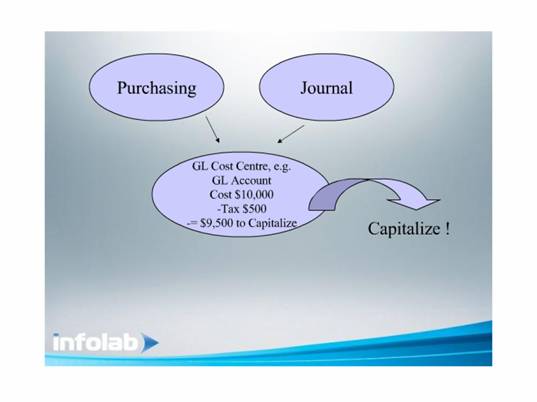

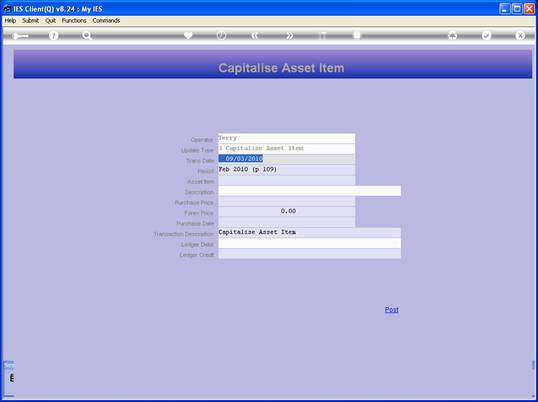

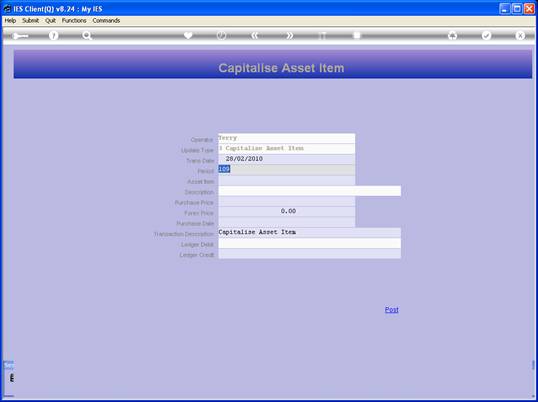

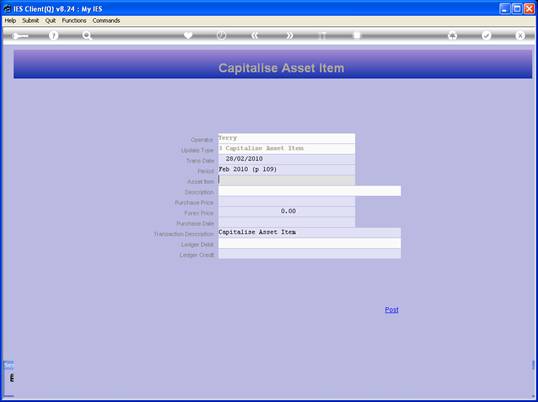

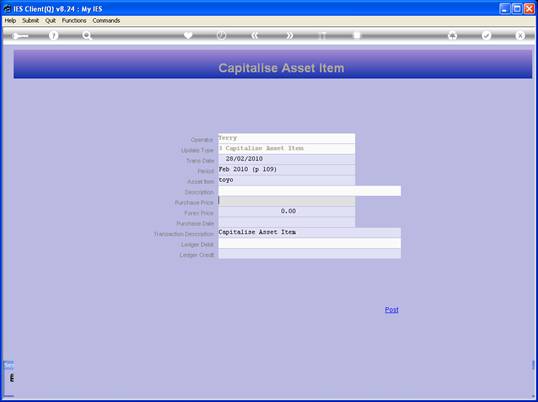

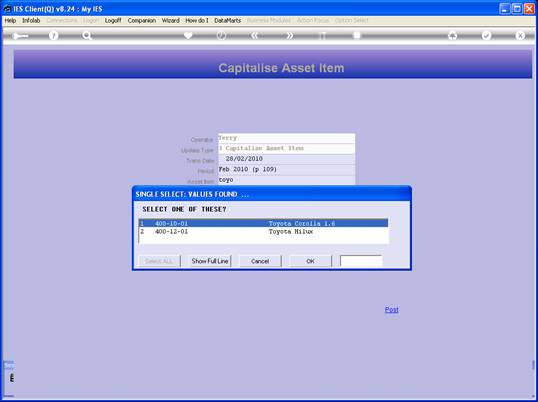

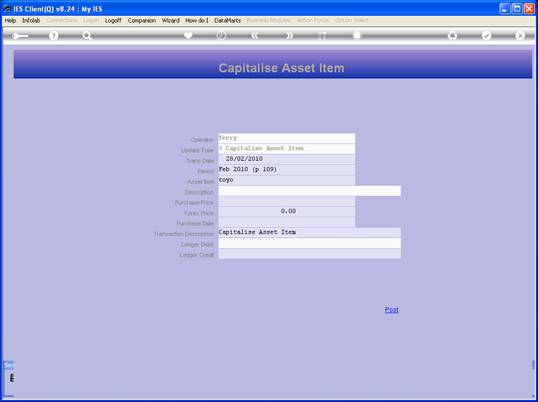

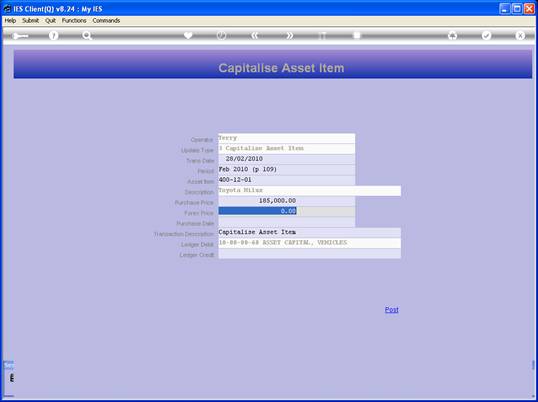

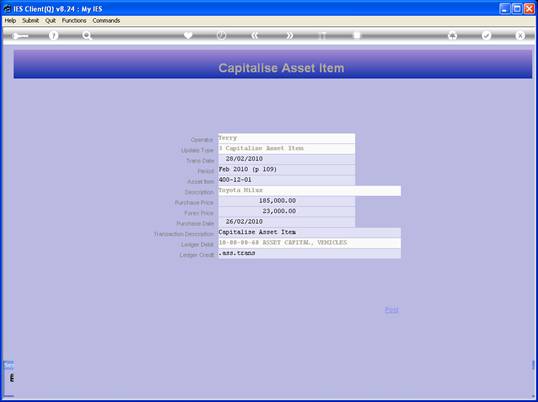

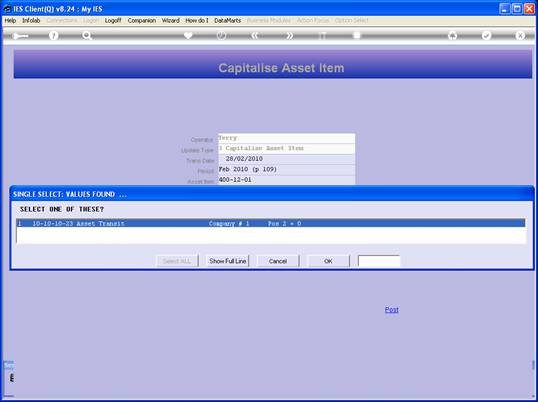

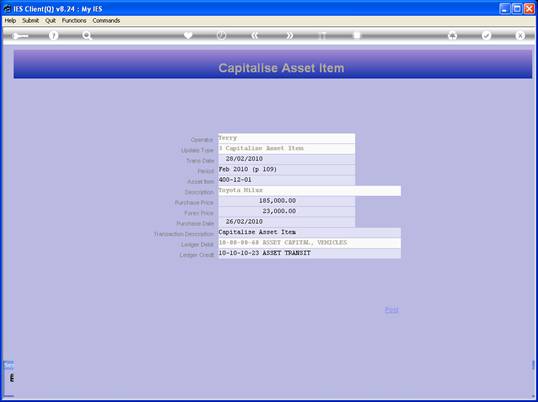

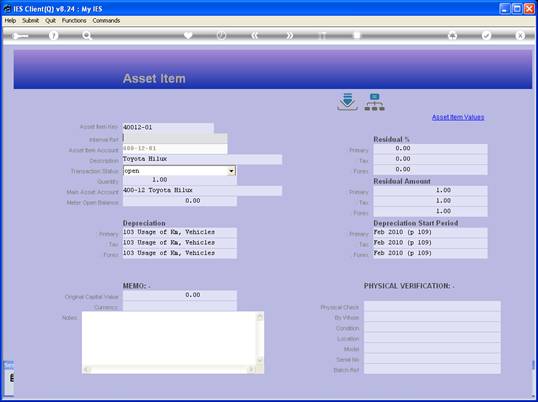

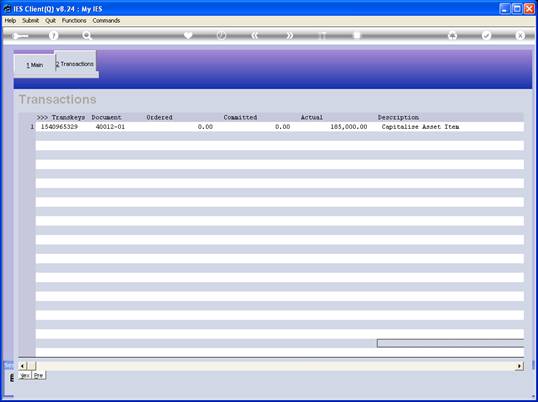

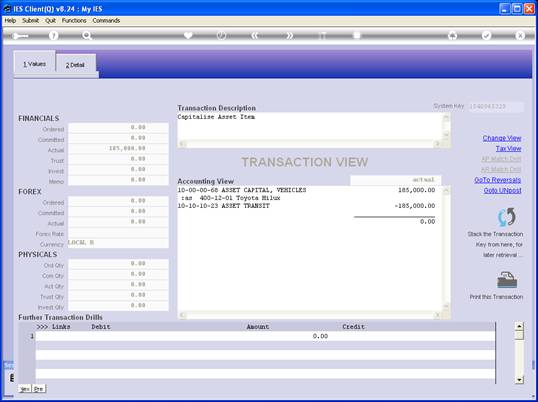

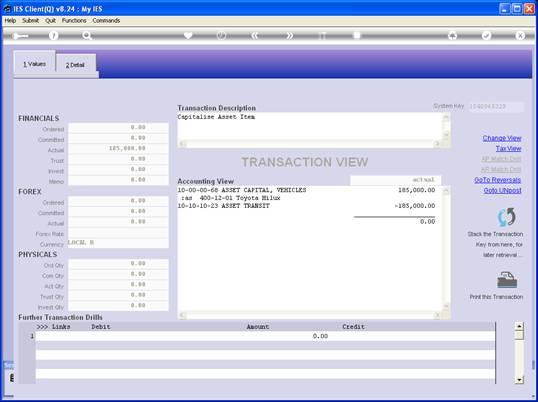

Slide notes: In this tutorial we will perform

an instance of Asset Capitalization. Whether the Asset is acquired through

Purchasing or by other means makes no difference to the process, because we

always Capitalize from a GL Account. Therefore, an Asset acquired through

Purchasing will have it's cost allocated in the 1st instance to some

Costing or Transit or Suspense Account, and if acquired in any other way,

the Cost will end up in an appropriate Account by Journal. Usually, in the

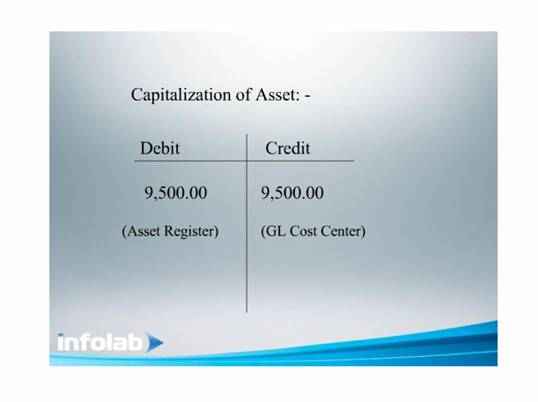

costing Account, the remaining Amount will already be net of Tax, as it is

usual to Capitalize an Asset net of Tax. Of course, there are some

exceptions to this rule.

|