|

Slide 5

Slide

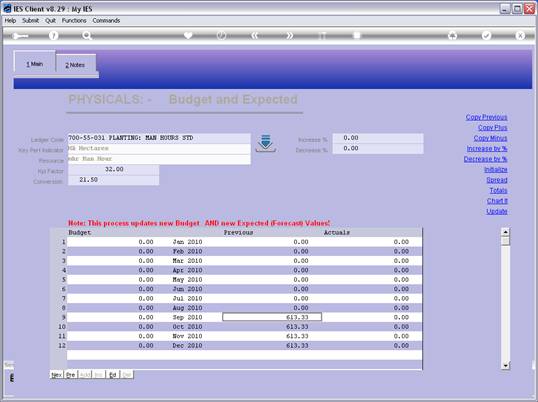

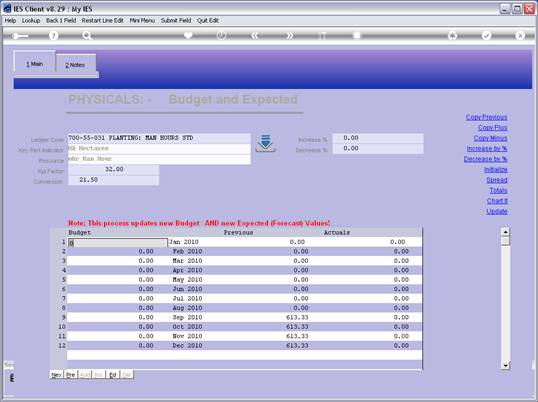

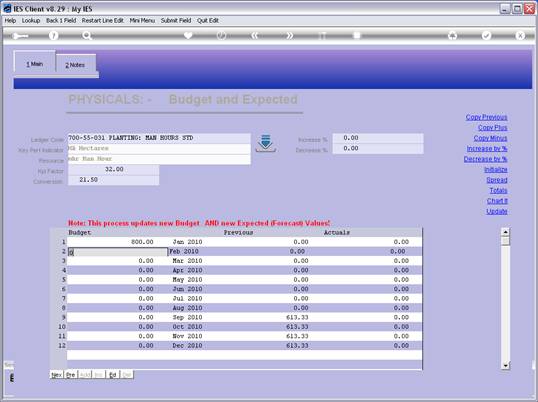

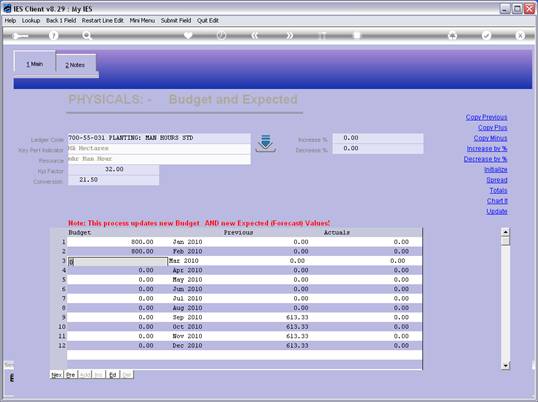

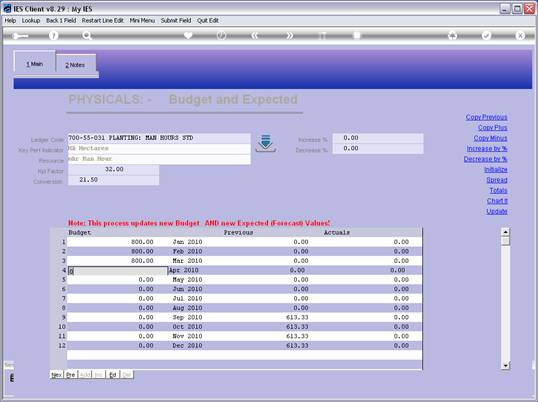

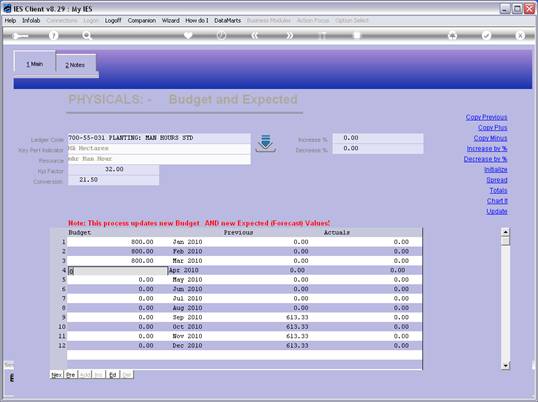

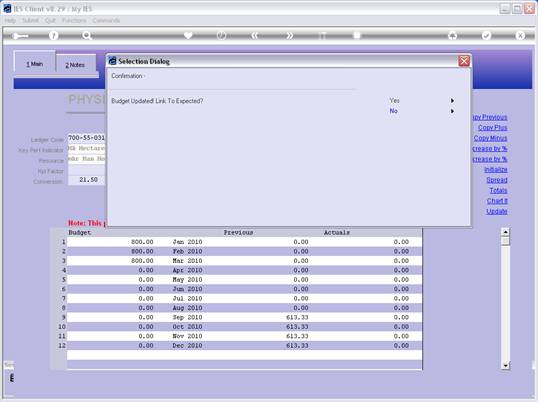

notes: From the tutorials on the Principles of Budget Capture, and with

regards to Physicals Budget Capture, we already know that the Physicals

Budget can be used with or without Resources and KPI's. For this Account,

we use it with Resource and KPI. Therefore, when we capture a Budget

quantity for this Account, it is not actually for Man Hours on this

Account, but rather for the number of Hectares, i.e. the KPI, that will be

planted, and therefore the Quantity will be used to calculate the required

Man Hours, based on the Hectares we wish to plant.

|