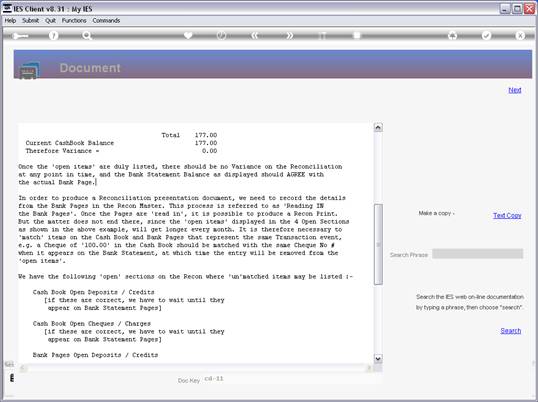

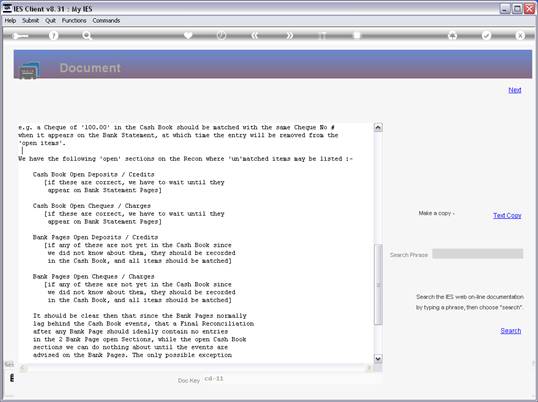

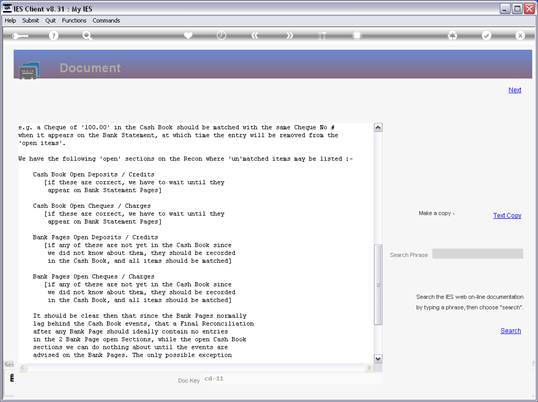

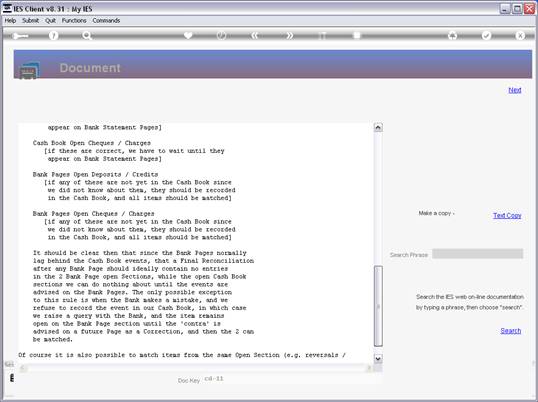

|

Slide 6

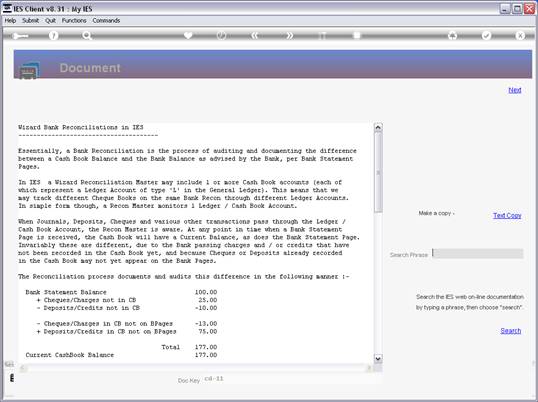

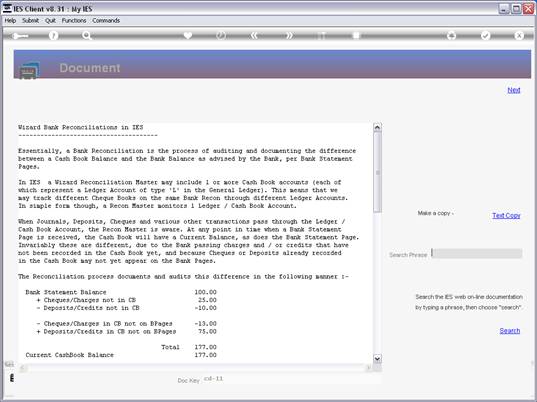

Slide notes: When we receive a Bank Statement,

the Balance is usually different from what our Cash Book shows. Why so?

Mostly it is because we post Deposits and Expenses in our Cash Book when

they are performed, but at the Bank these Deposits may not show up immediately

on the Bank Page, and especially the Cheques may take longer to arrive for clearance

at the Bank and may only show up on our Statement much later. Then there

are also Charges from the Bank, and Stop Orders and Debit Orders that we may

only become aware of when we receive the Bank Statement, and that we do not

have in our Cash Book yet.

|