|

Slide 18

Slide notes:

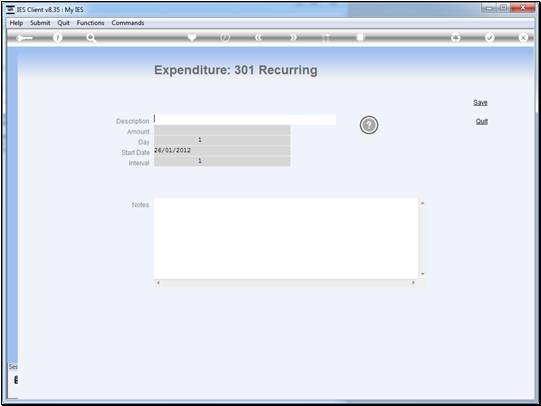

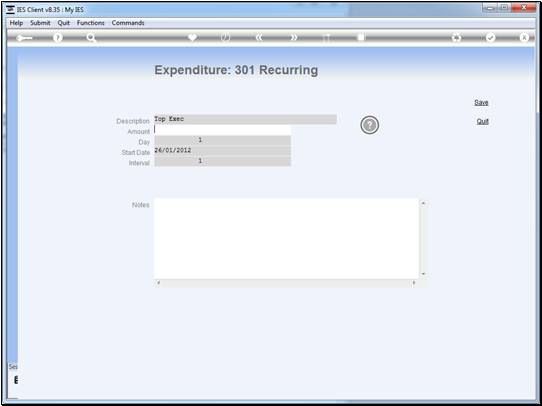

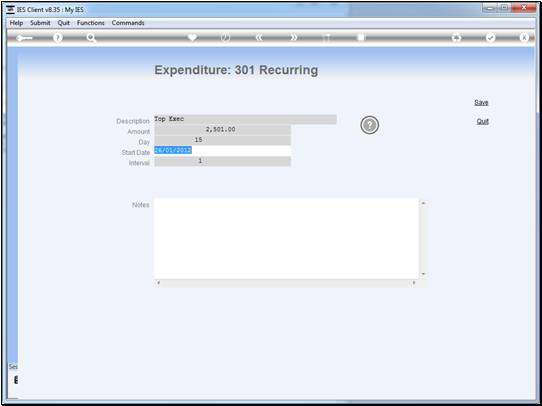

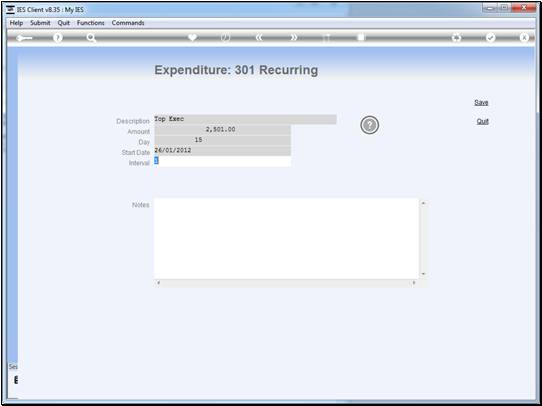

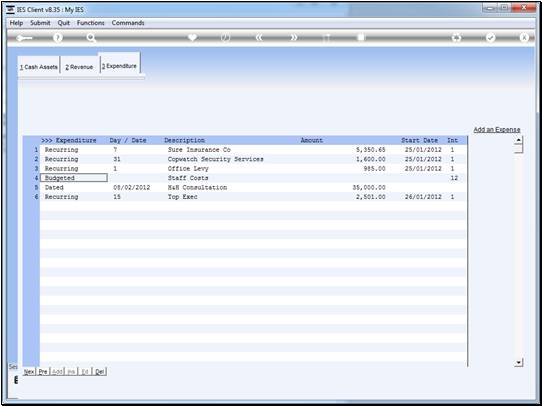

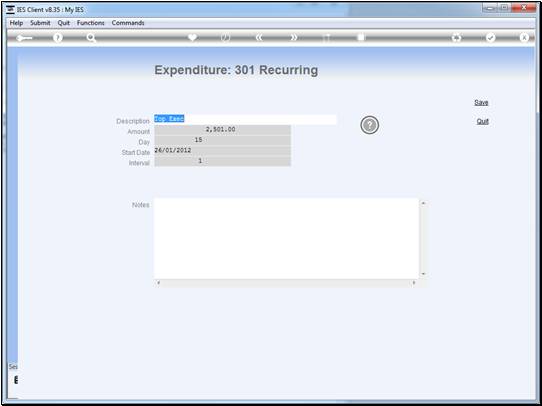

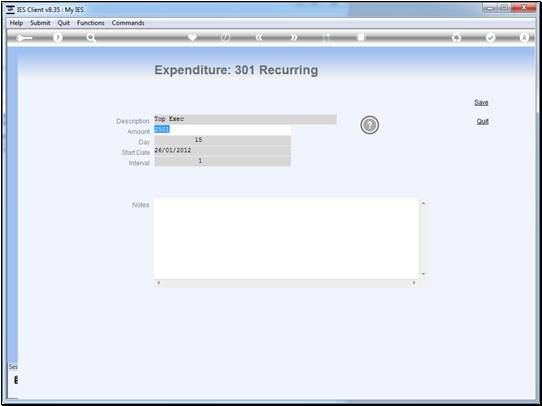

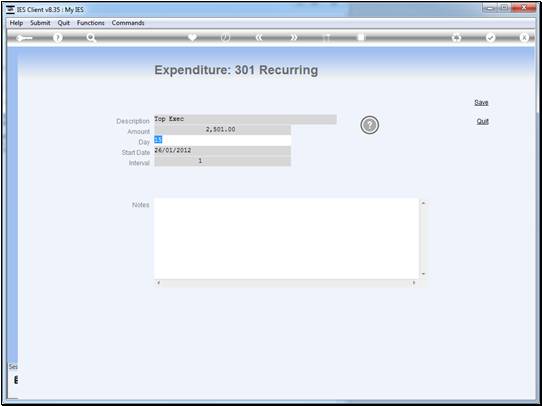

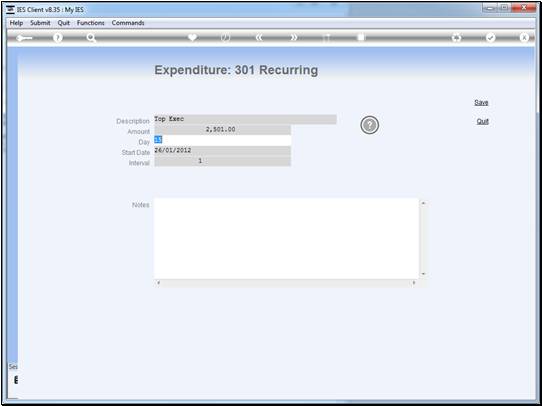

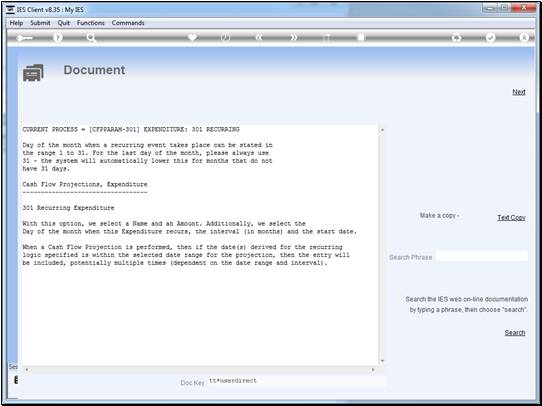

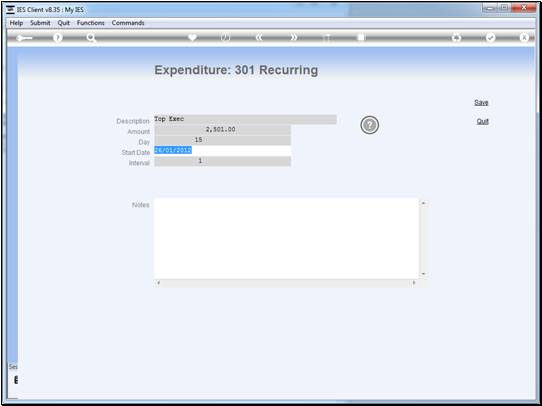

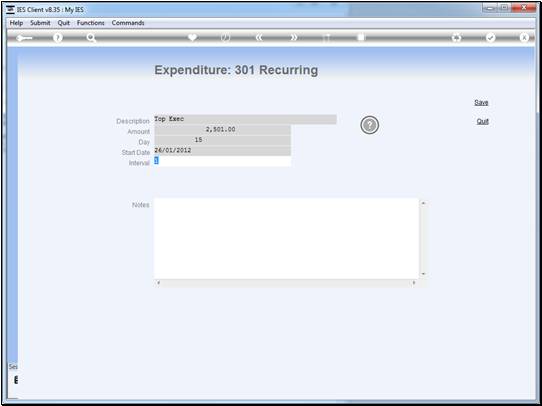

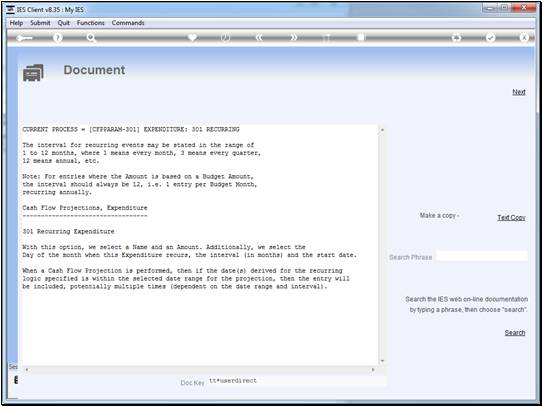

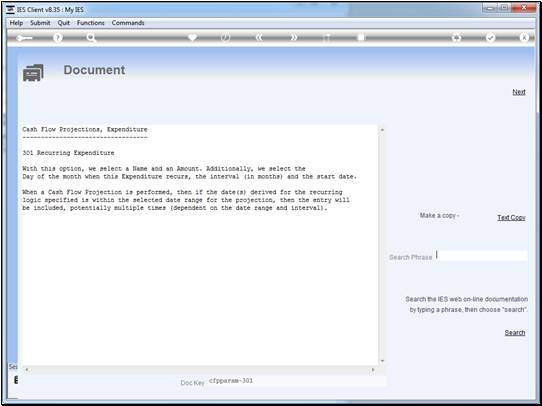

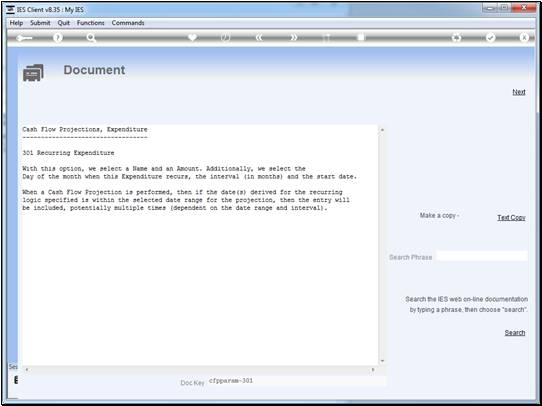

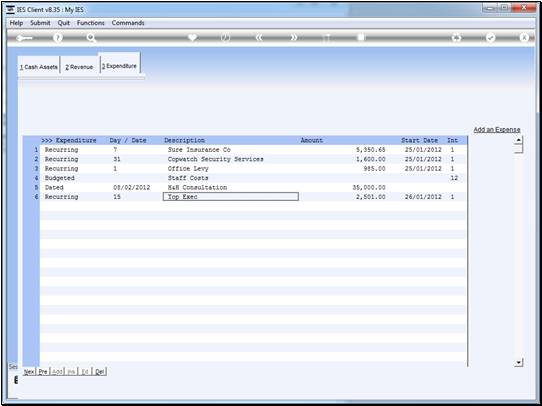

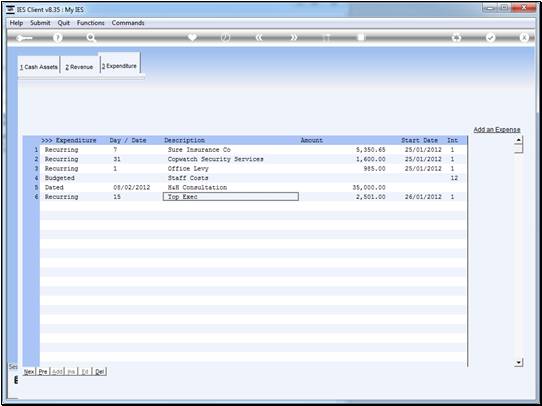

The start date is indicated only for the system to learn at which month the

Recurring Expense starts. Then, from the selected interval in months, the

system will also know when the Expense should recur. Therefore, depending

on the date range when the projection is performed, this entry can result

in multiple occurrences.

|