Slide

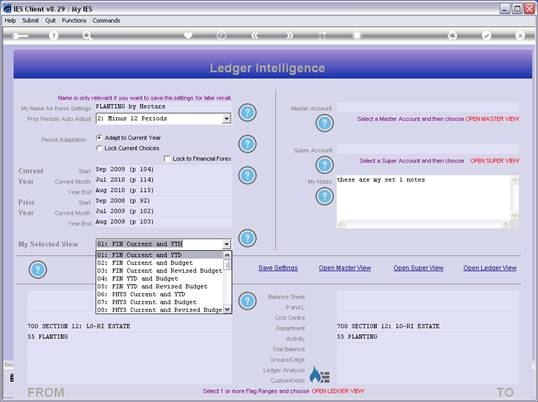

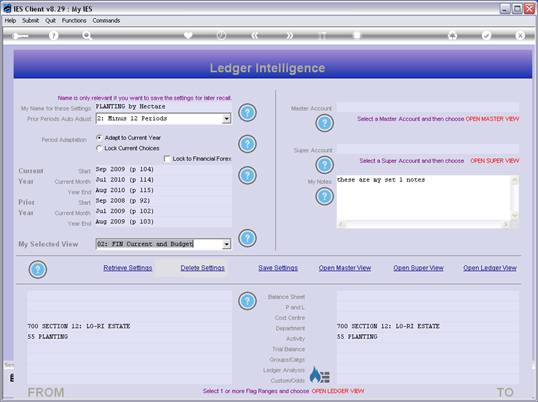

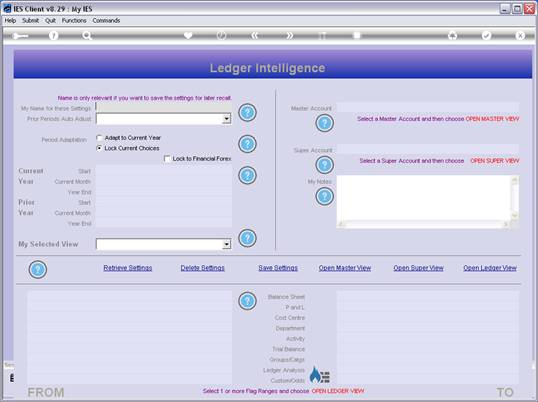

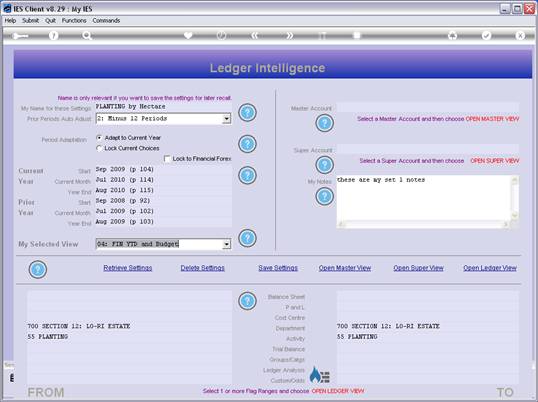

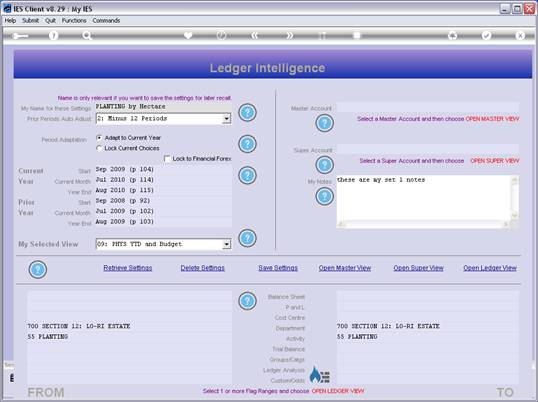

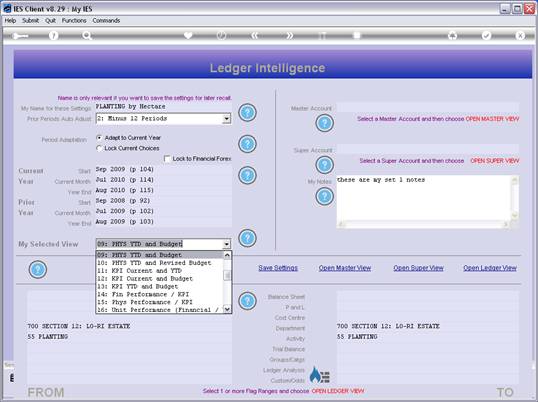

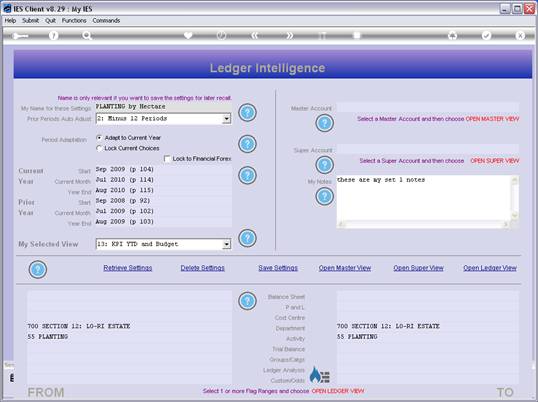

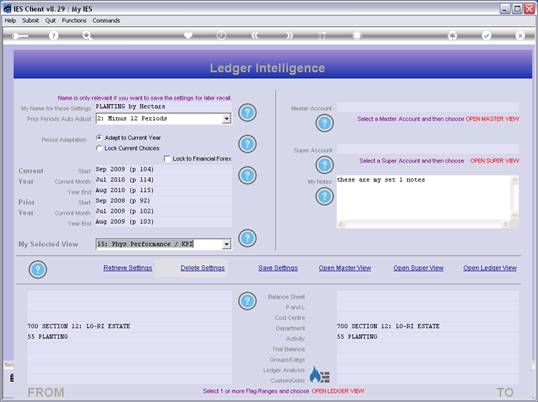

notes: We speak of the View that we select for the comparative results as

the "inner" View within the View, because apart from the various

methods for gathering the Accounts that will be used for the Result, there

are also an entire series of different measurements available. And the

selected measurement is the so-called "inner view".

Slide 2

Slide

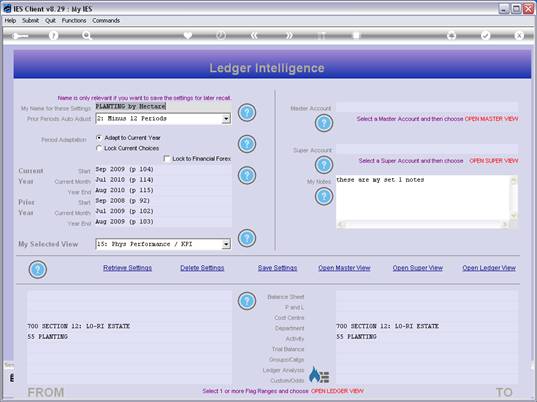

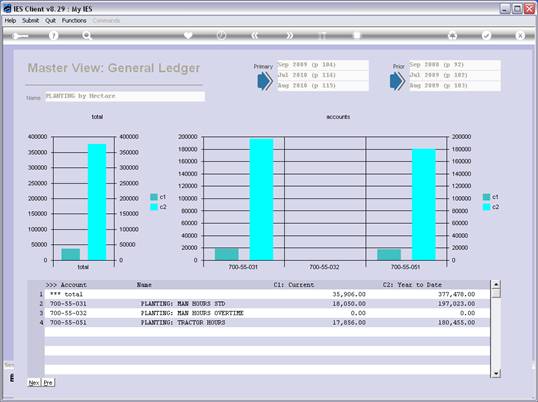

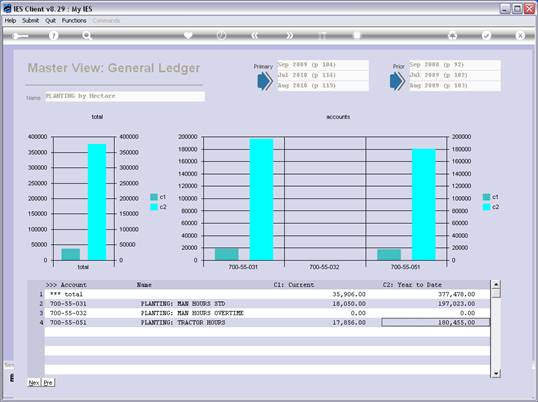

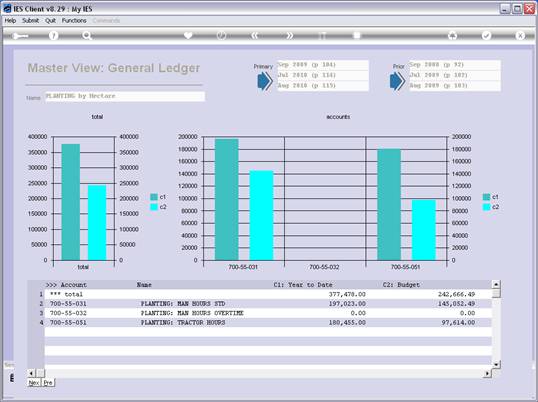

notes: In this example, we are looking at results of Planting on a certain

section of an Estate, which is also called Department 700 in the Chart of

Accounts. From all the Accounts in this Department, we are focusing

specifically on those Accounts that relate to the Planting Activity.

Slide 3

Slide

notes:

Slide 4

Slide

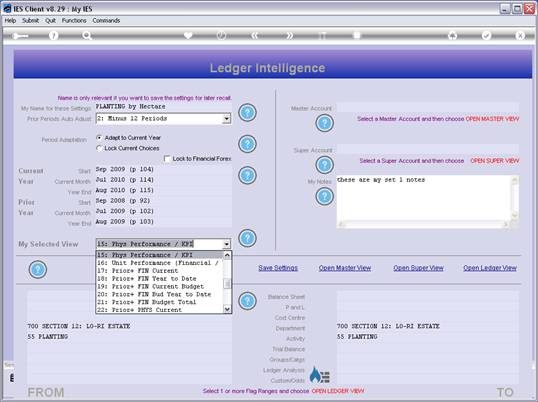

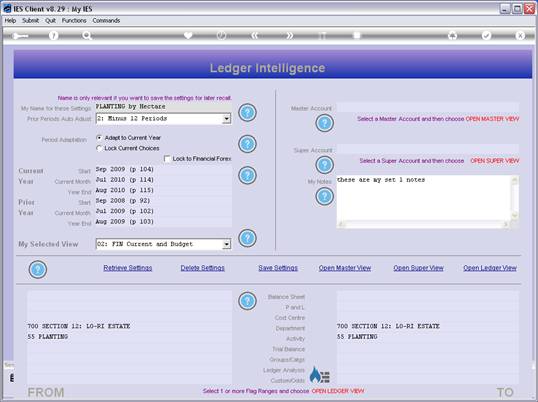

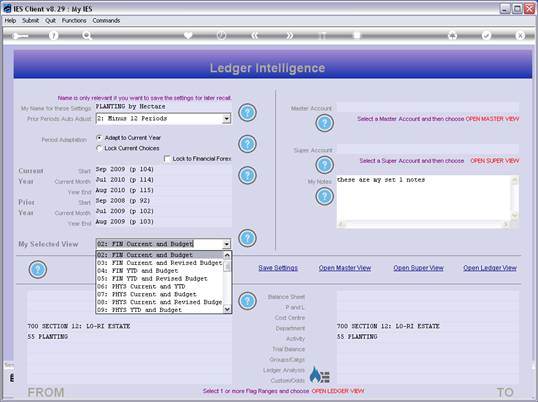

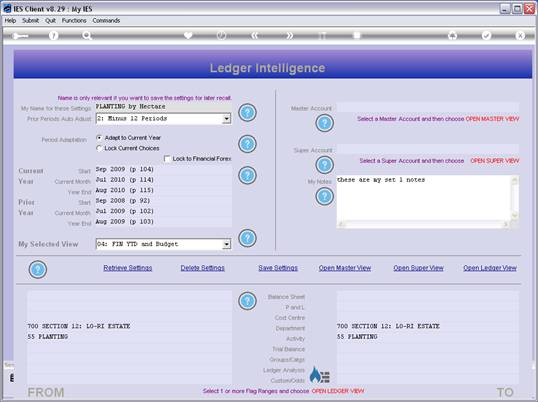

notes: So let us first select the measurement or inner view number 1, which

will reveal Financial results for the selected Current Month and Year to

Date.

Slide 5

Slide

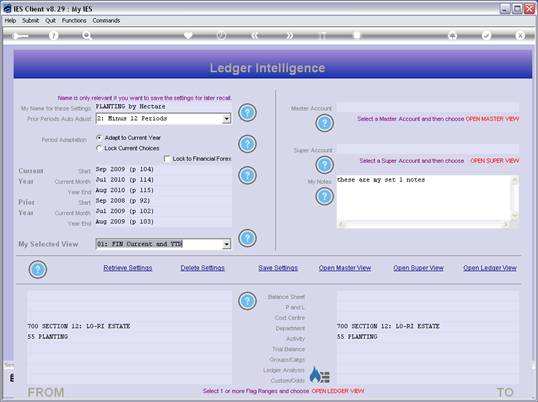

notes: Here is the View.

Slide 6

Slide

notes:

Slide 7

Slide

notes:

Slide 8

Slide

notes:

Slide 9

Slide

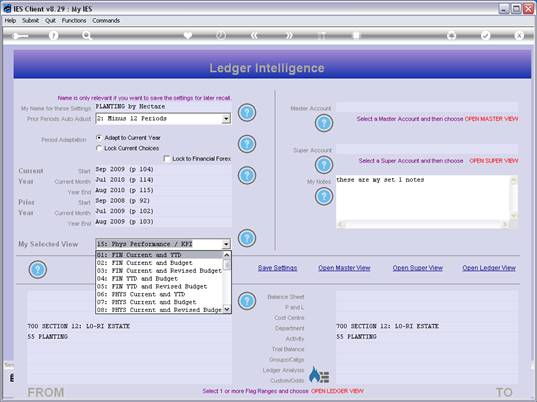

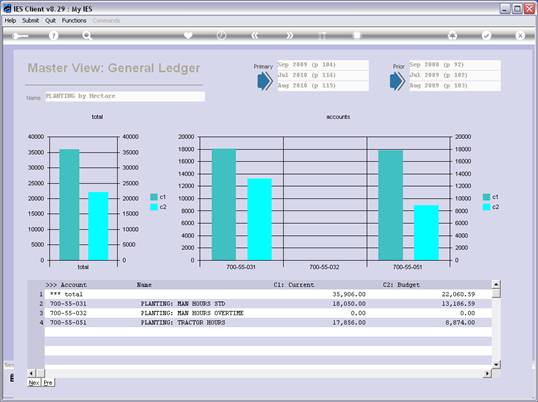

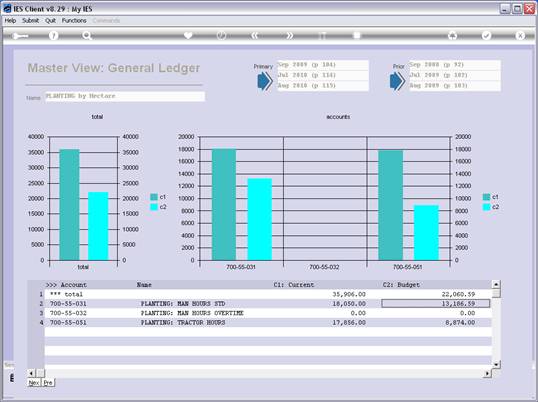

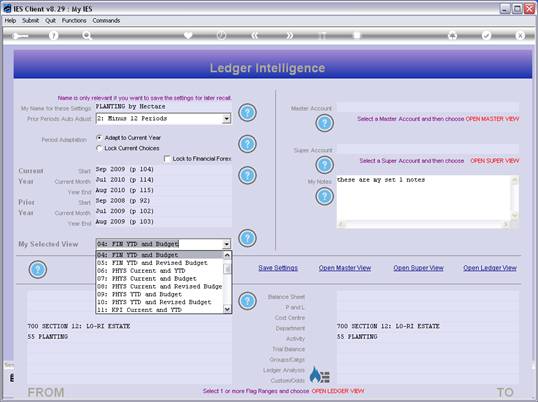

notes: Next, we use View number 2 to reveal the Current Month Financial

performance versus the Financial Budget.

Slide 10

Slide

notes: And theresult is that we are

significantly overspent. We may ask the question why this is so.

Slide 11

Slide

notes:

Slide 12

Slide

notes:

Slide 13

Slide

notes:

Slide 14

Slide

notes:

Slide 15

Slide

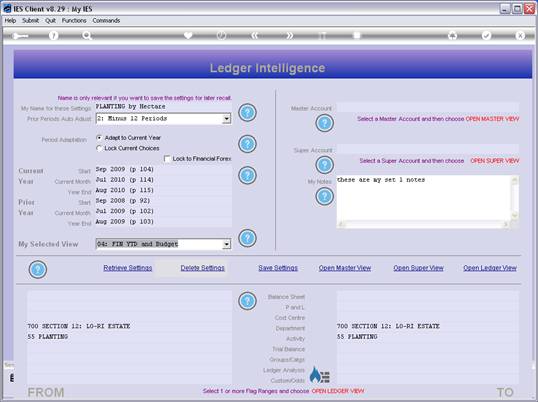

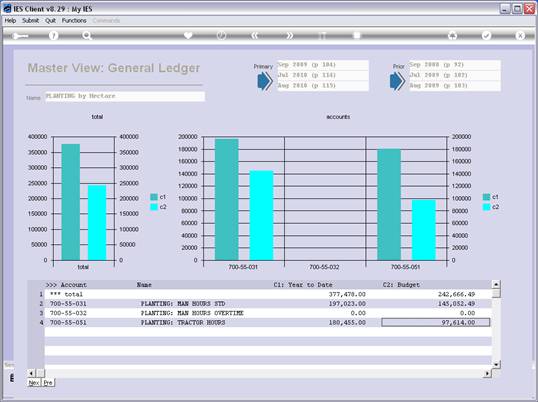

notes: View number 4 will show us what the Year to Date Financial

performance is versus the Budget.

Slide 16

Slide

notes: And here again, we are seriously overspent.

Slide 17

Slide

notes:

Slide 18

Slide

notes:

Slide 19

Slide

notes:

Slide 20

Slide

notes:

Slide 21

Slide

notes:

Slide 22

Slide

notes: So we may ask, what is the Physical performance versus the Budget,

because that will reveal the Management performance on the ground, whereas

the Financial over expenditure may be beyond the Section Manager's control

due to Price escalation over which he has little or no control, but the

Physical performance is certainly within his control.

Slide 23

Slide

notes: And here we see quite a different picture. We are still over Budget,

but only slightly, and nothing like on the Financial level. So that is

interesting, and begs the question whether perhaps we have Planted more

than planned?

Slide 24

Slide

notes:

Slide 25

Slide

notes:

Slide 26

Slide

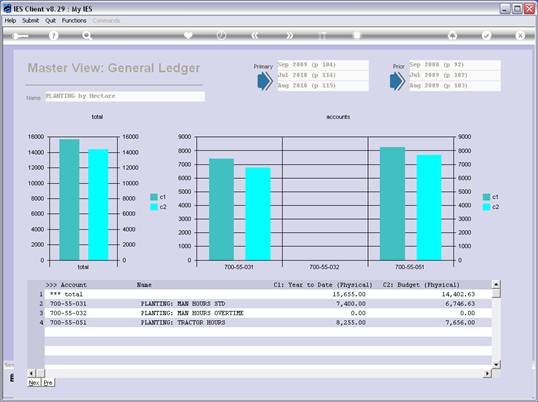

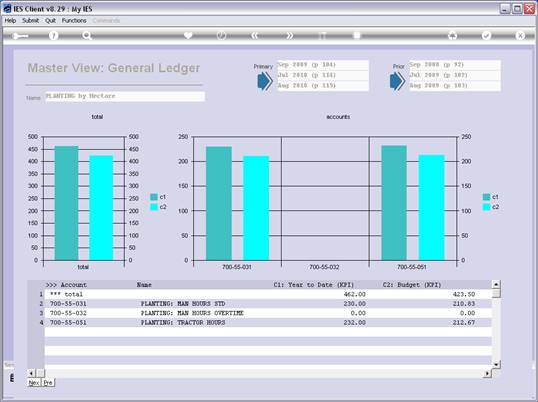

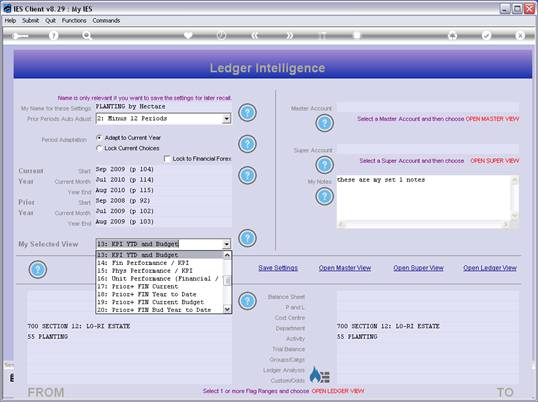

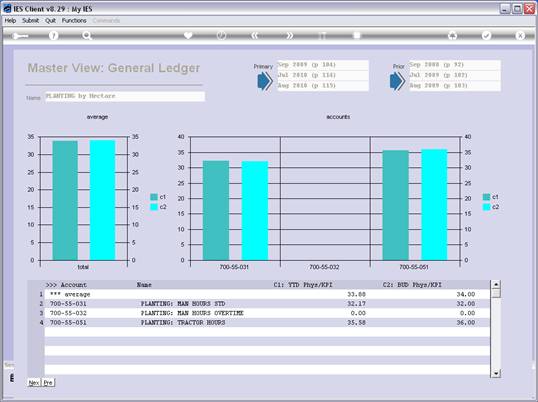

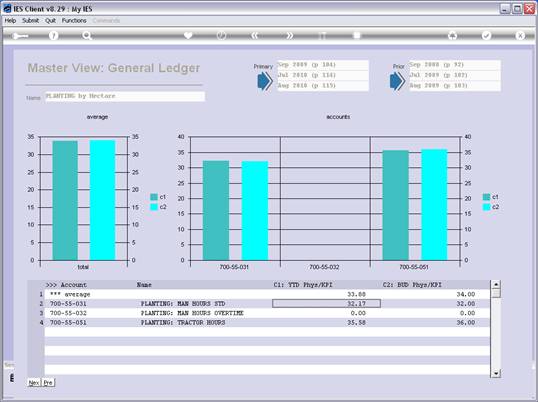

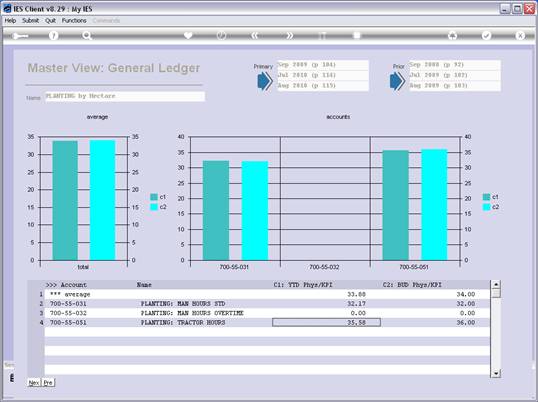

notes: So next we choose view number 13, which will reveal the Year to Date

Key Performance Indicator versus Budget. In other words, we will be able to

find out how many Hectares we have Budgeted to Plant, and how many we have

actually planted.

Slide 27

Slide

notes: Sure, the answer is that we have planted roughly 20% more Hectares

than originally Budgeted for, hence the Physical being slightly over

Budget. As such, there must be another reason why the Financial is so

heavily overspent, and we can already deduce that it is not related to the

Physical performance, but to some other reason.

Slide 28

Slide

notes:

Slide 29

Slide

notes:

Slide 30

Slide

notes:

Slide 31

Slide

notes:

Slide 32

Slide

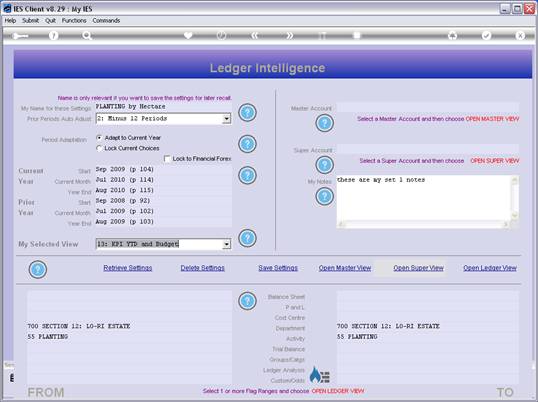

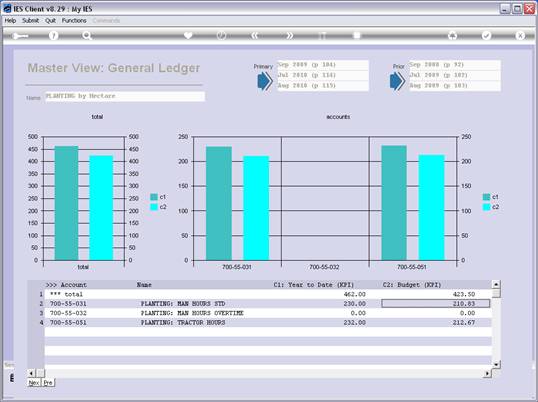

notes: To double-check the Physical Performance, we choose view 15, which

will reveal the Physical Performance over KPI.

Slide 33

Slide

notes: The result, as we can see, is good. It means that the standard

number of Man Hours per Hectare planted is only slightly exceeded, and the

Tractor Hours applied per Hectare planted is below the standard, hence an

excellent performance.

Slide 34

Slide

notes:

Slide 35

Slide

notes: And so, as we can see from this example, we can use the Measurement

Views productively to find the answers we want about our Business, whatever

kind of Business it is. Our example here has been Agriculture, but the same

principles can be applied in any Business, with the Business Intelligence

tools that we have here.