|

Slide 55

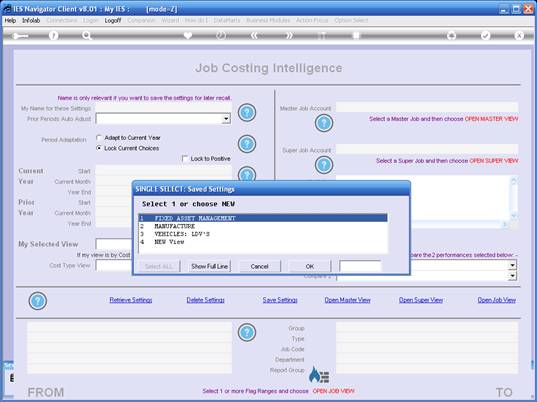

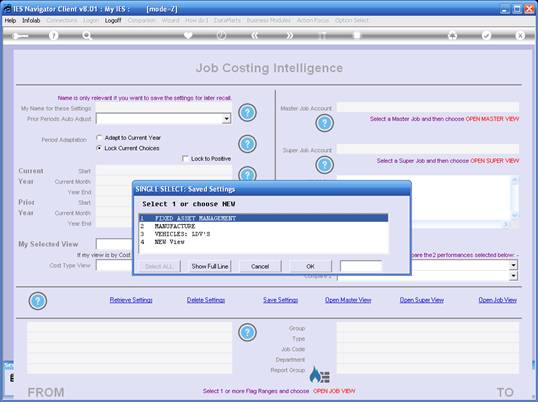

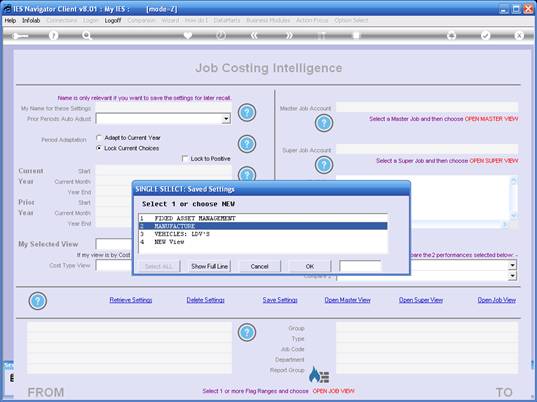

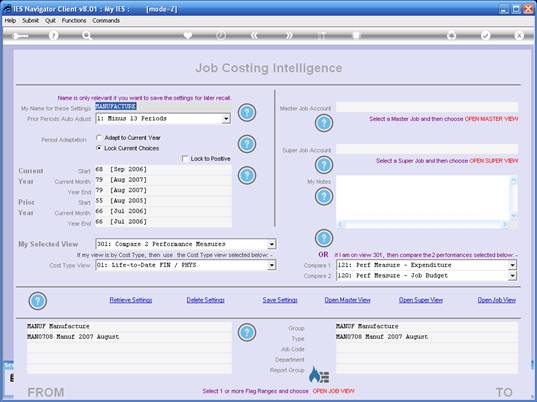

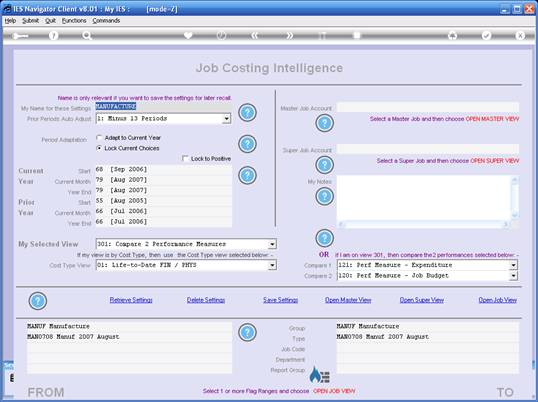

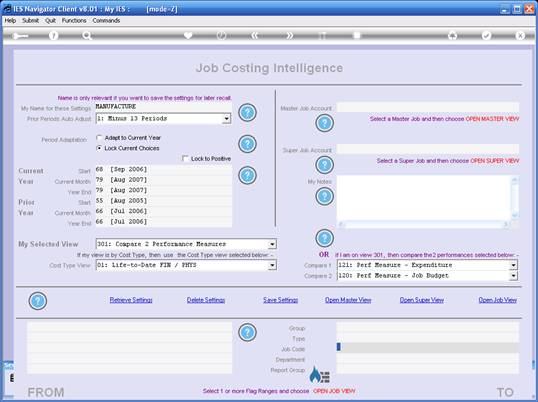

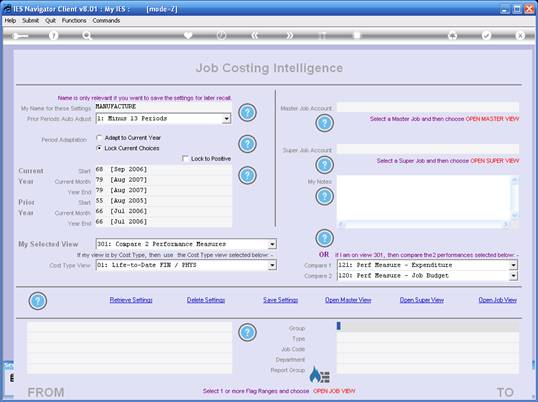

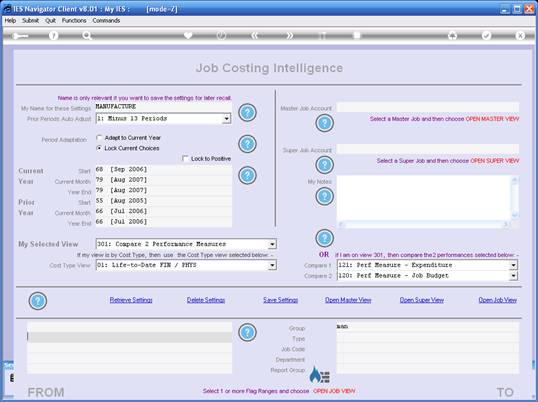

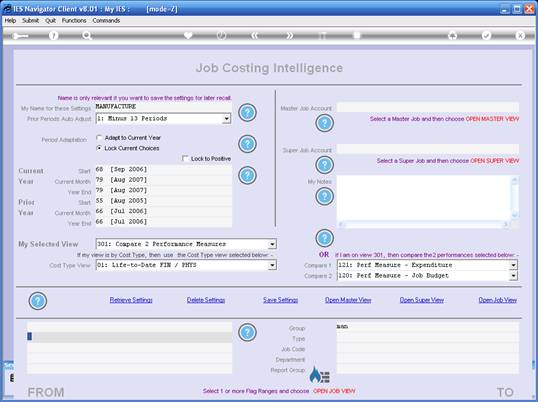

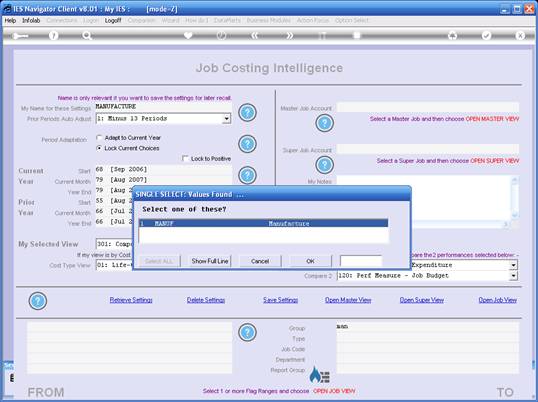

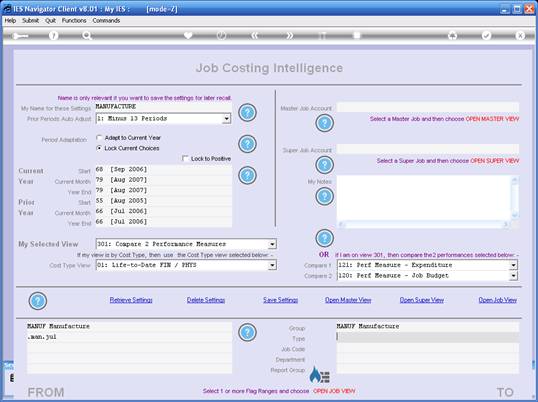

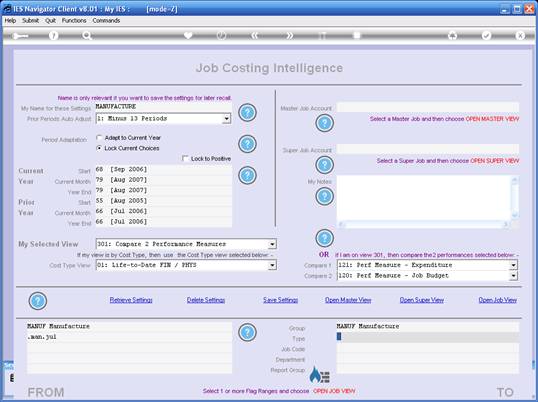

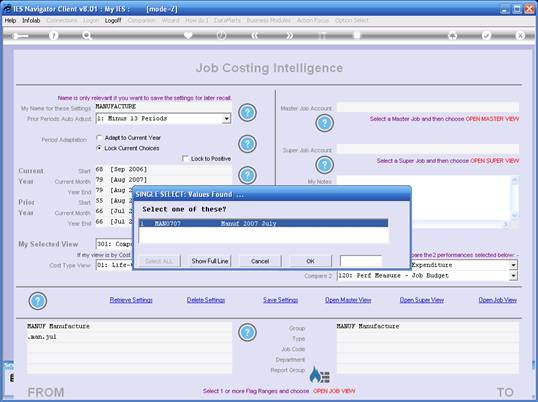

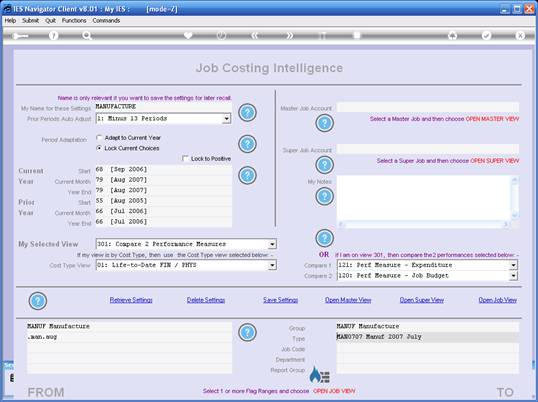

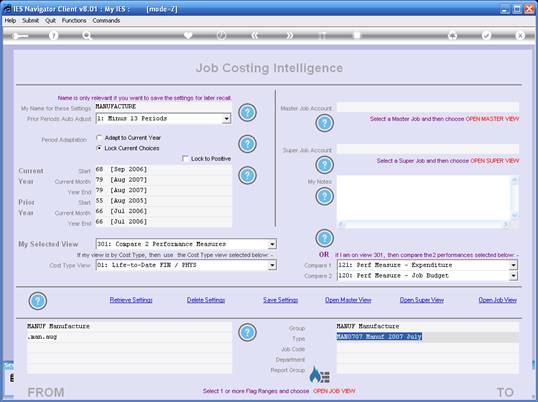

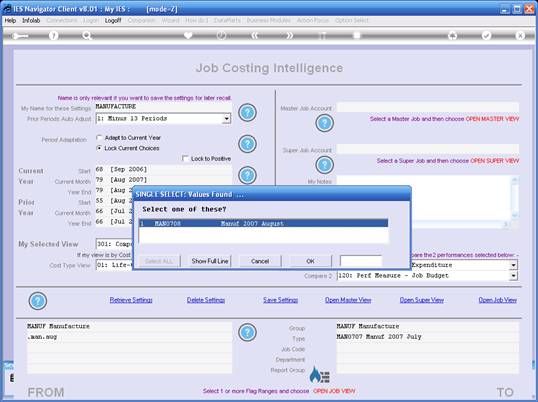

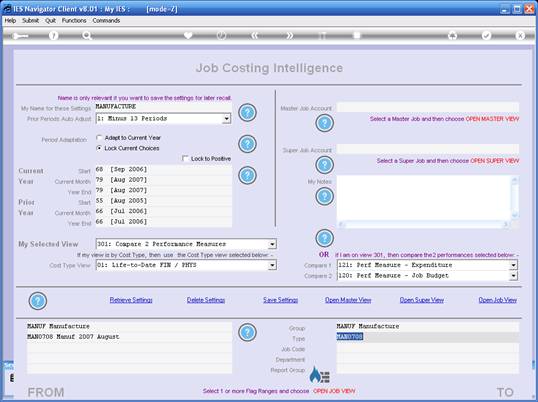

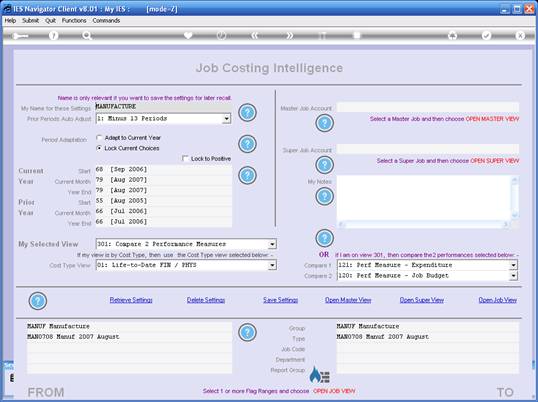

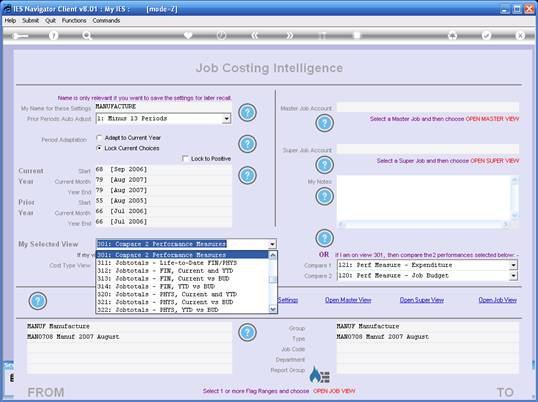

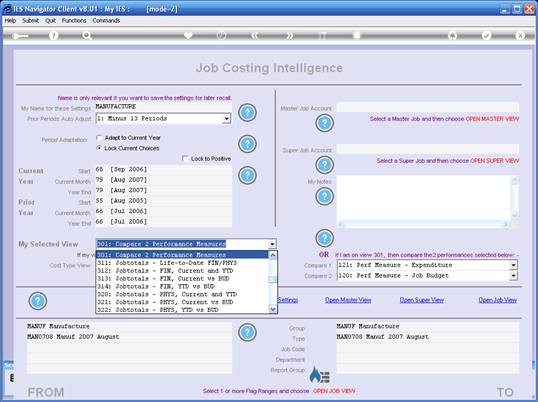

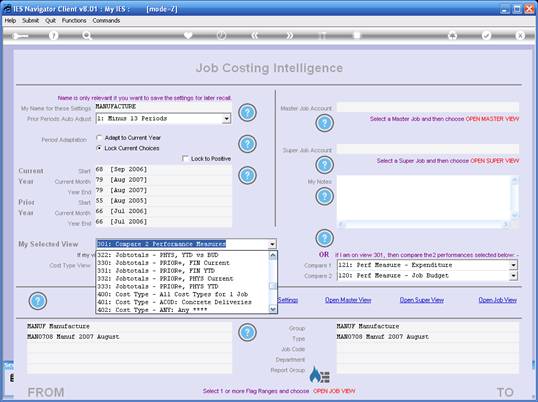

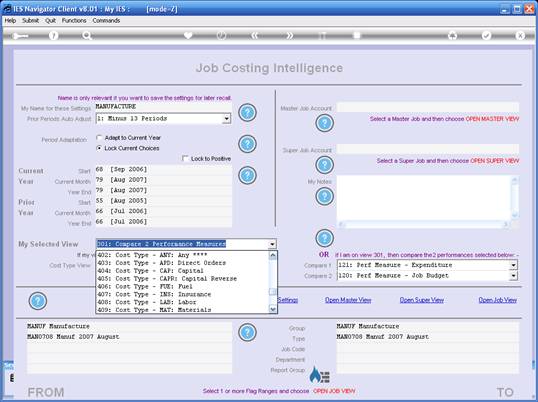

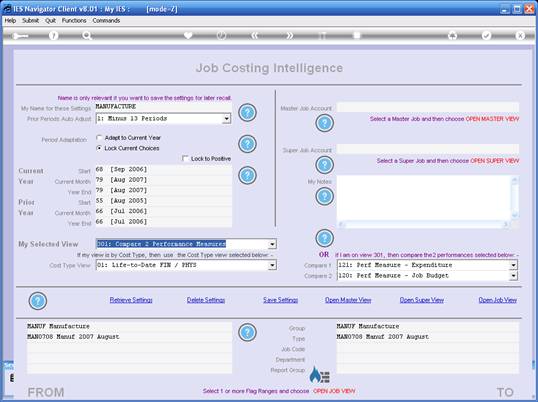

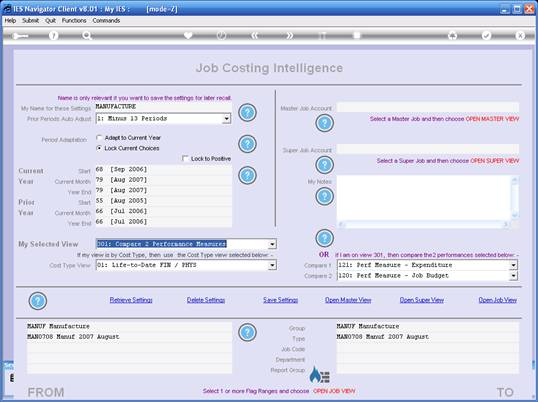

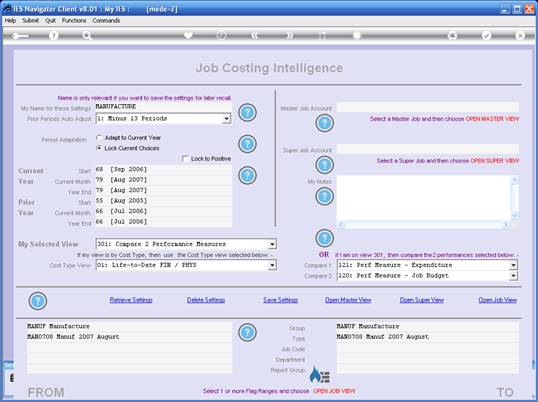

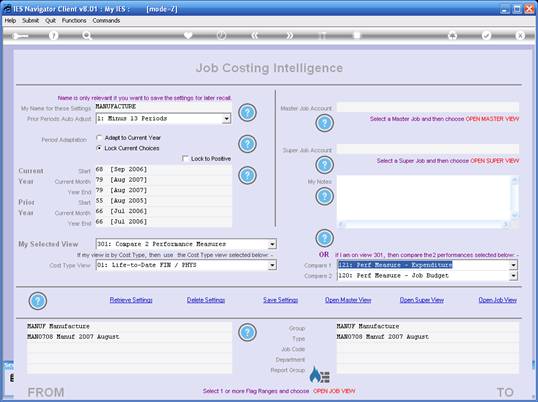

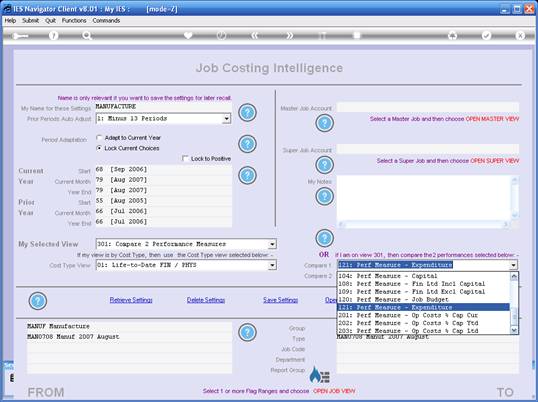

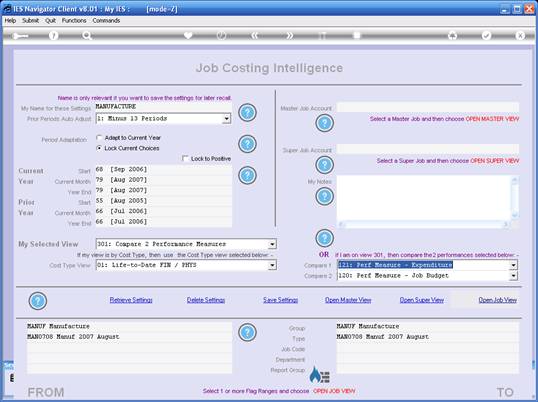

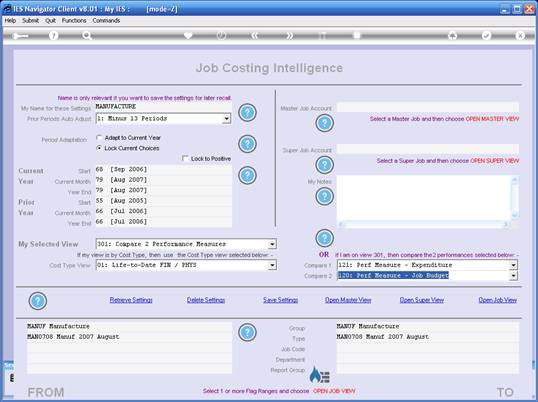

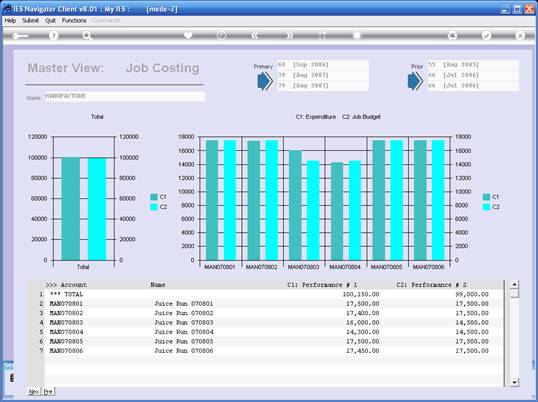

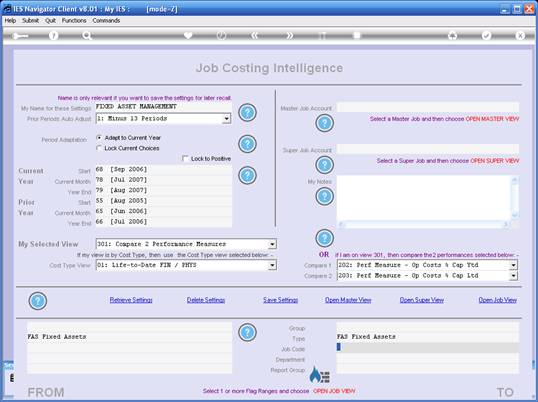

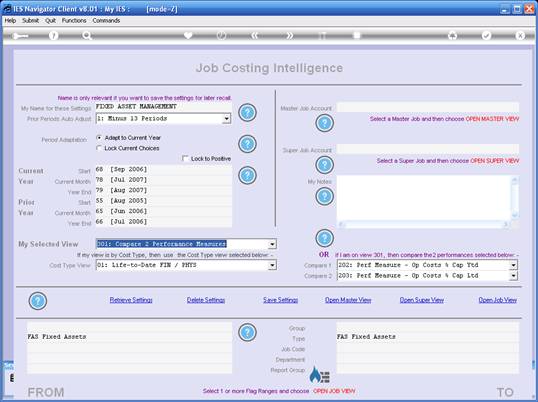

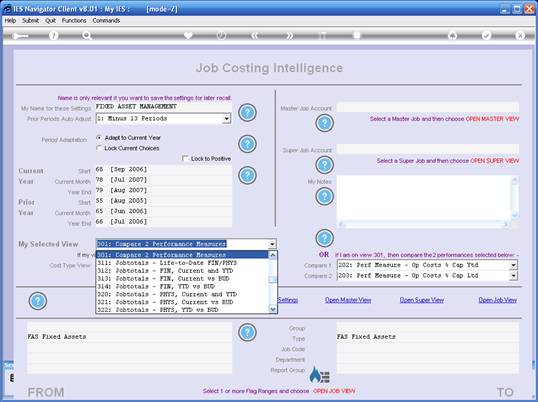

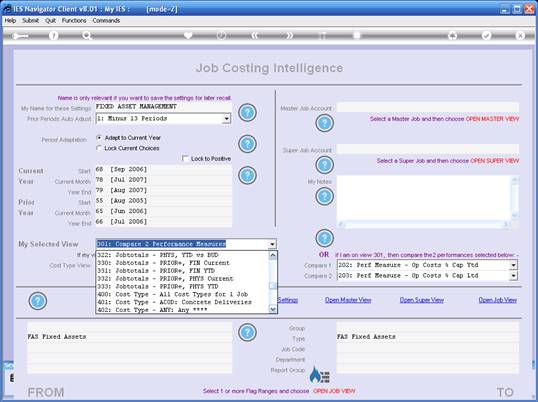

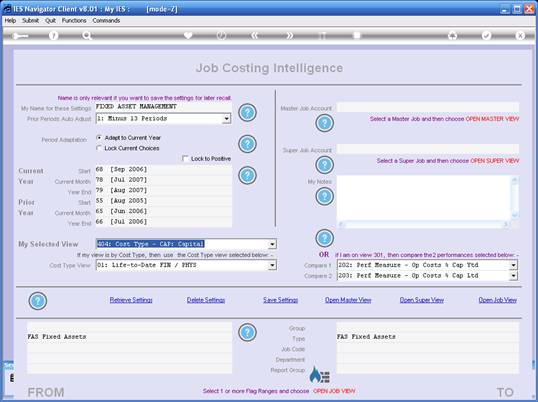

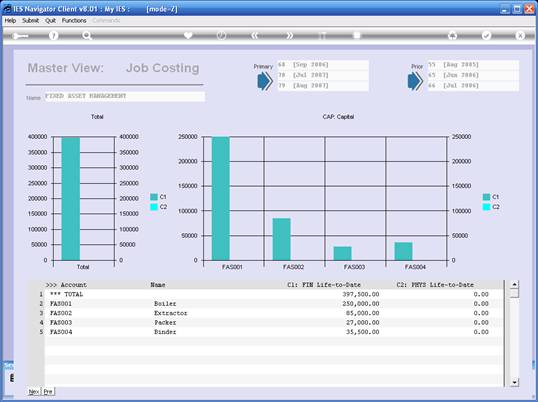

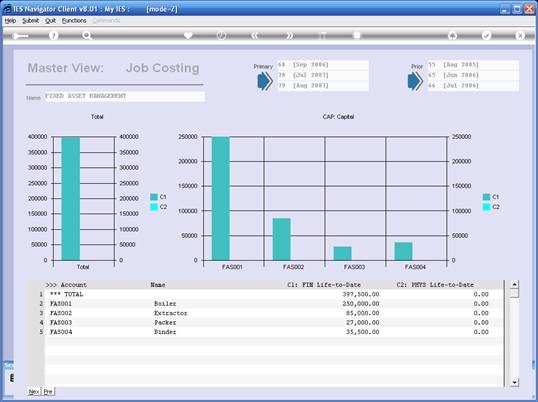

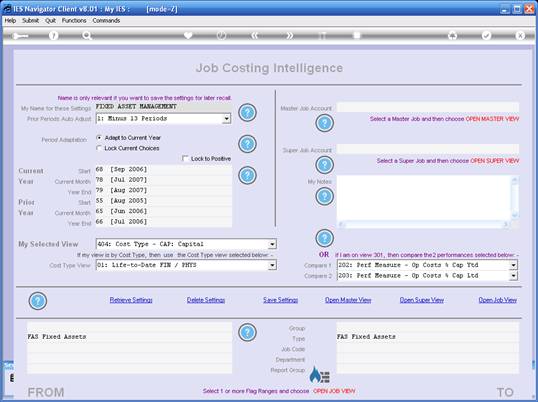

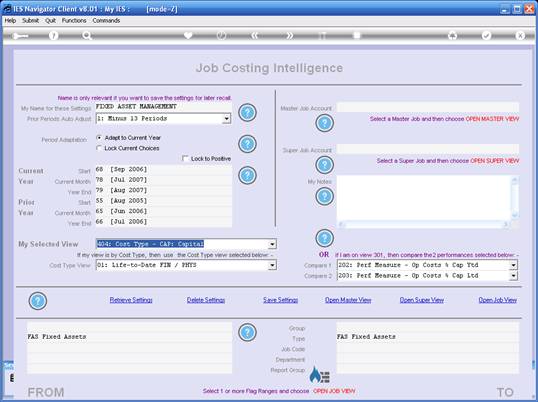

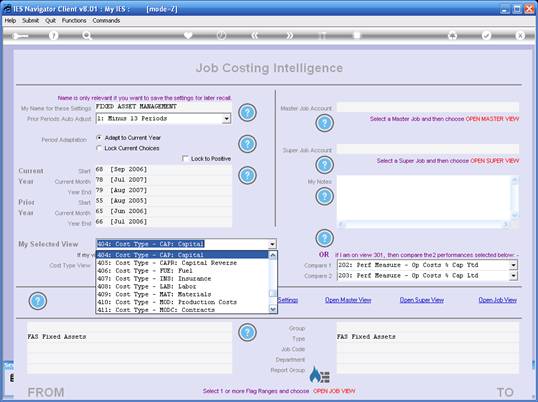

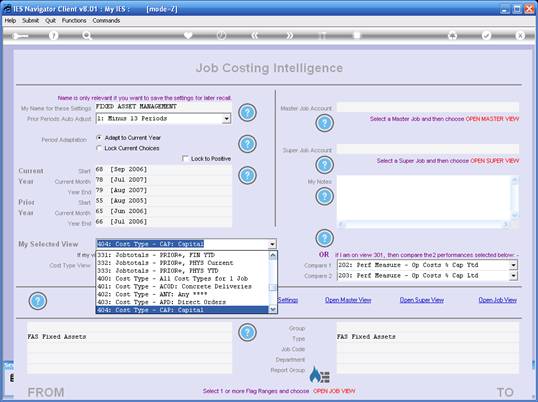

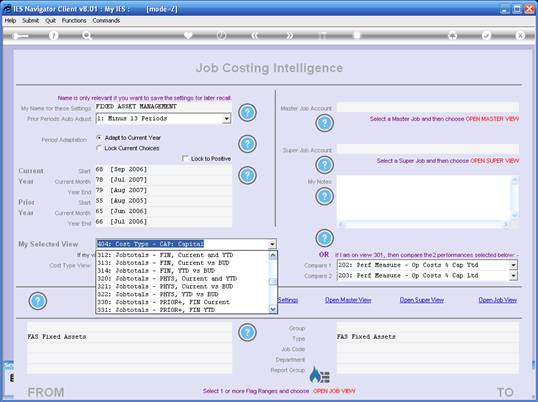

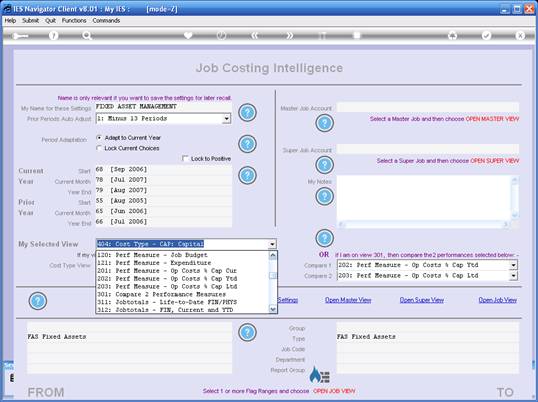

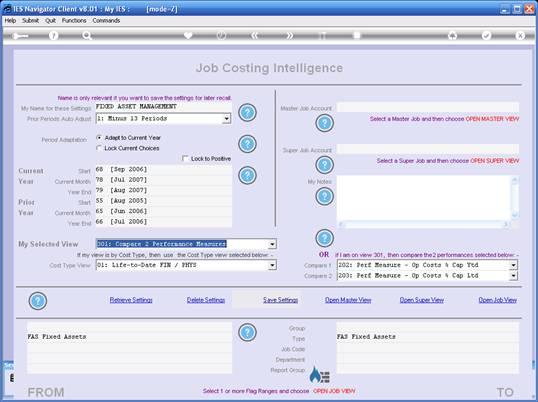

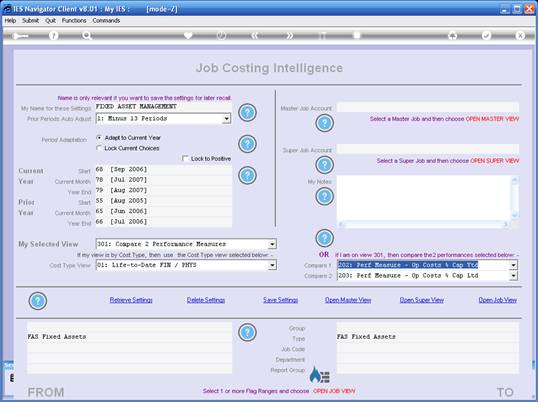

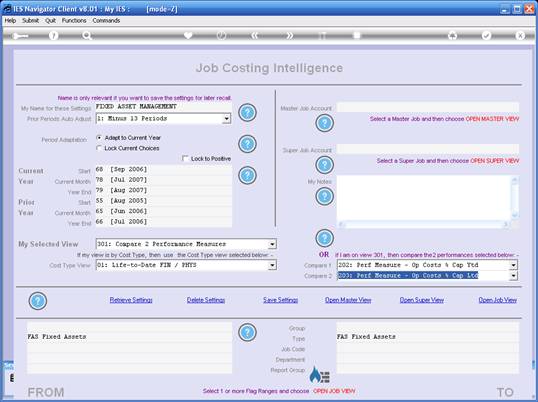

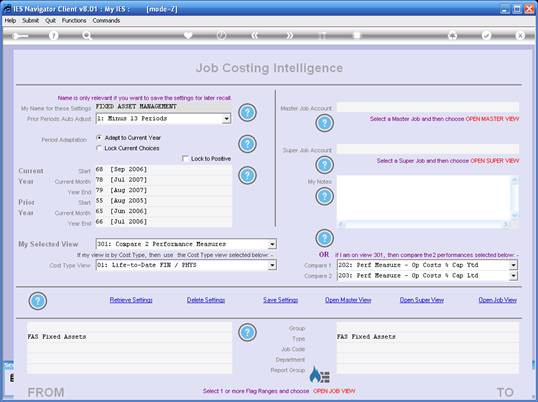

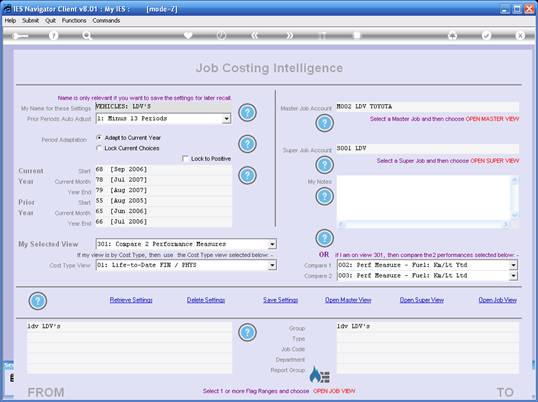

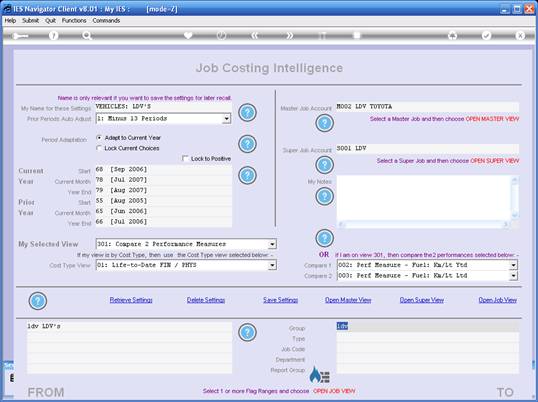

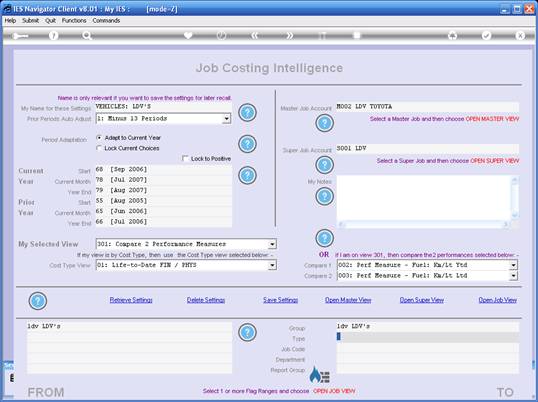

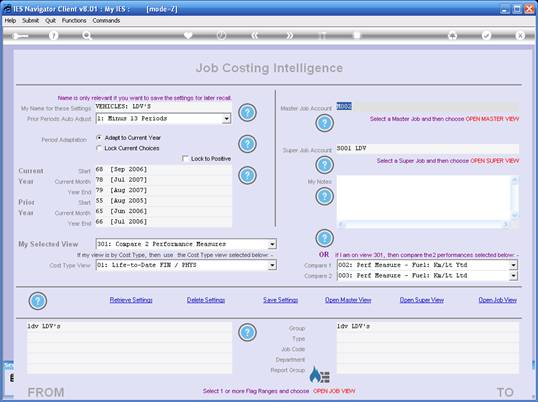

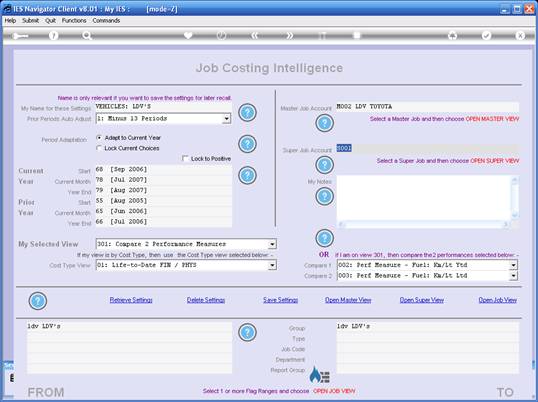

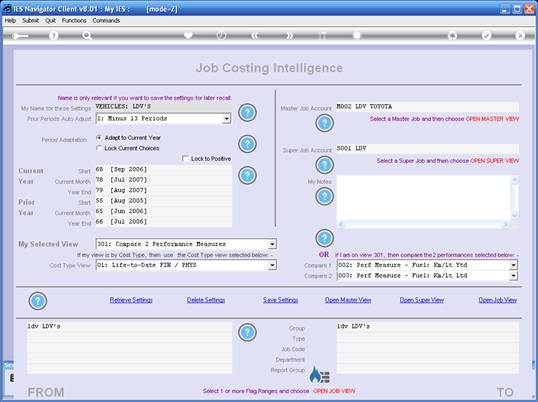

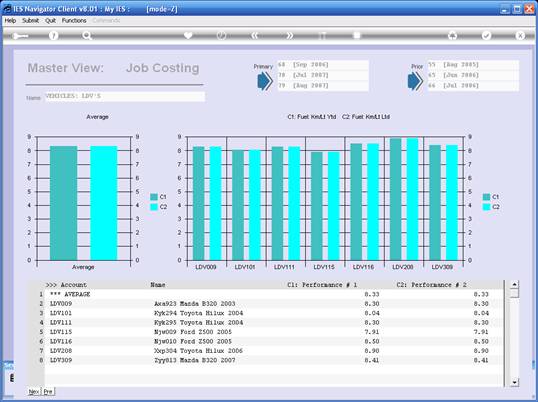

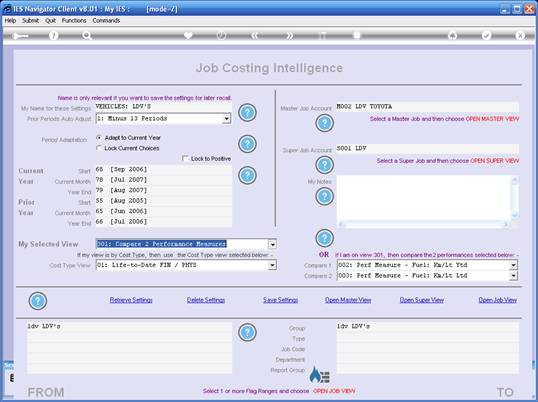

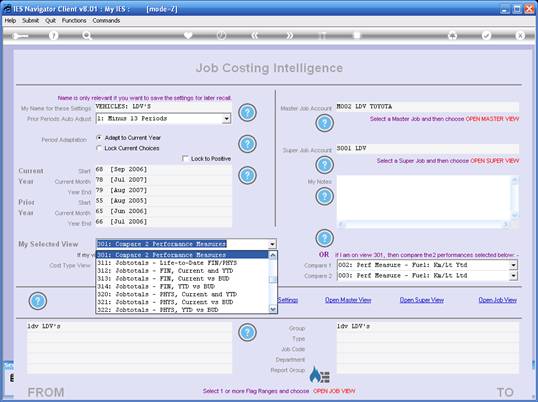

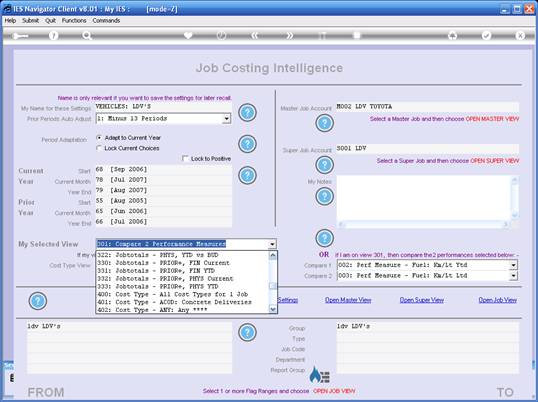

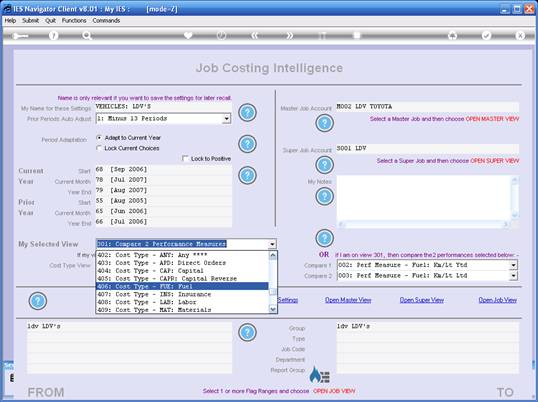

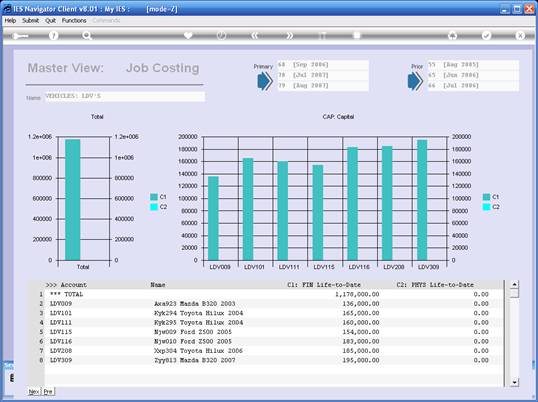

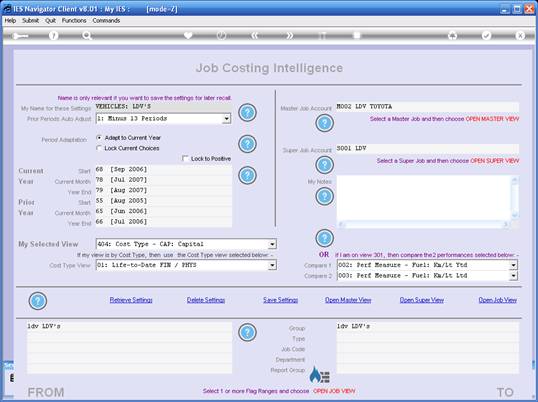

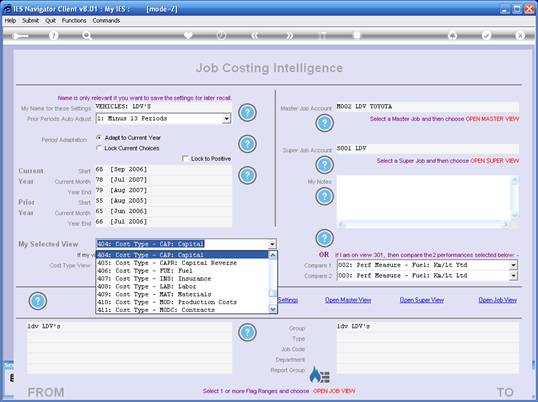

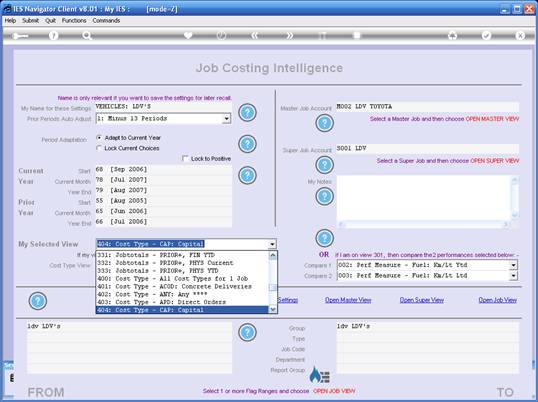

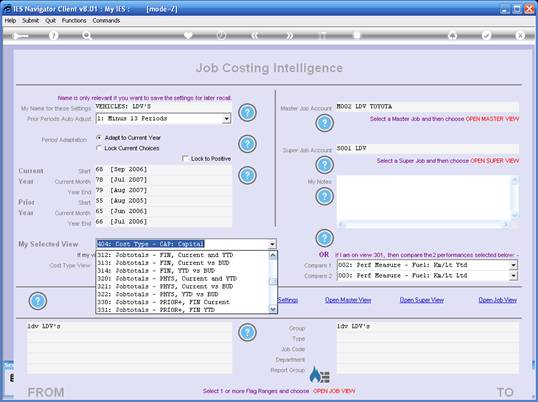

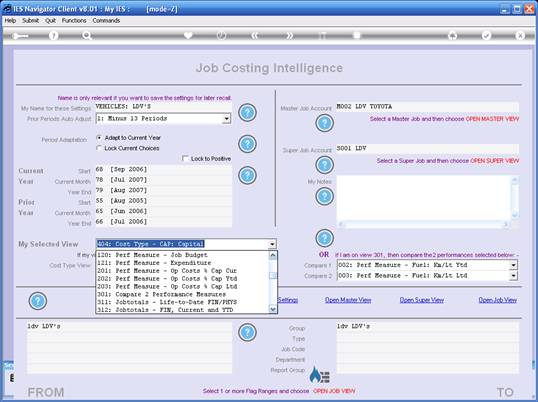

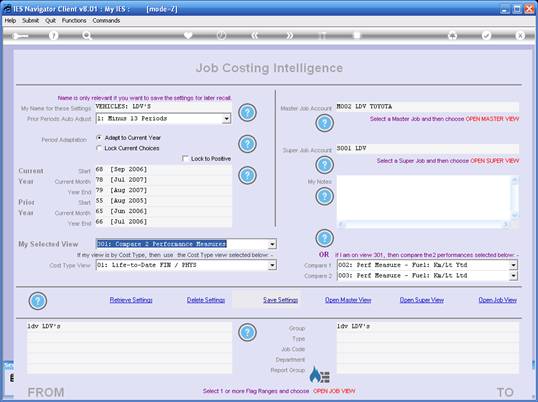

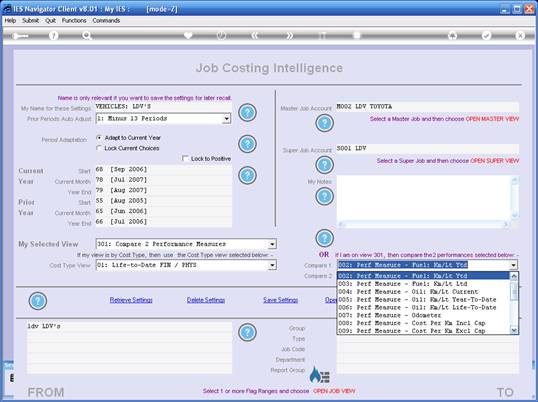

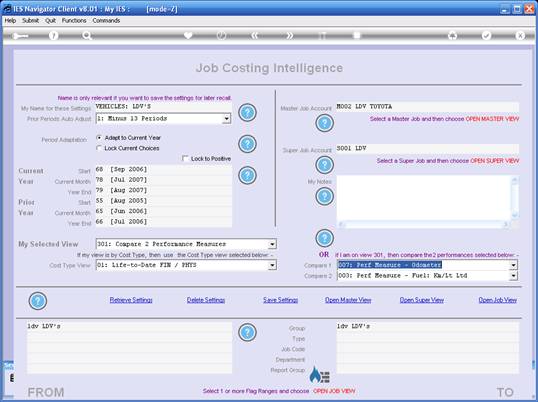

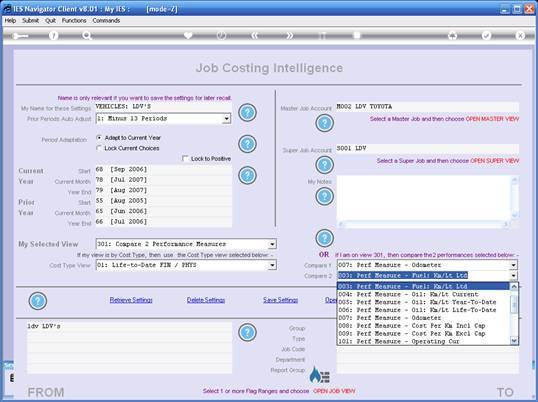

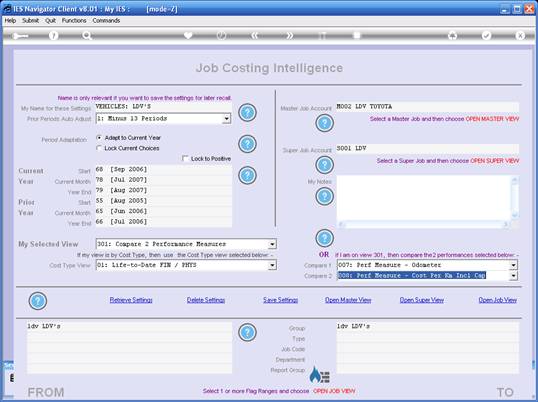

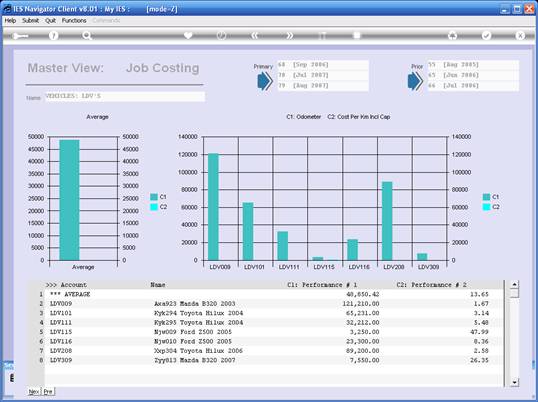

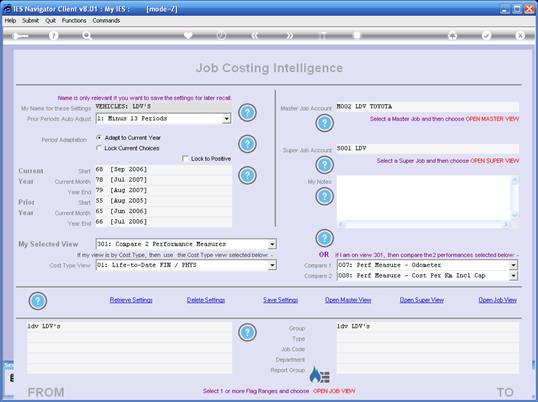

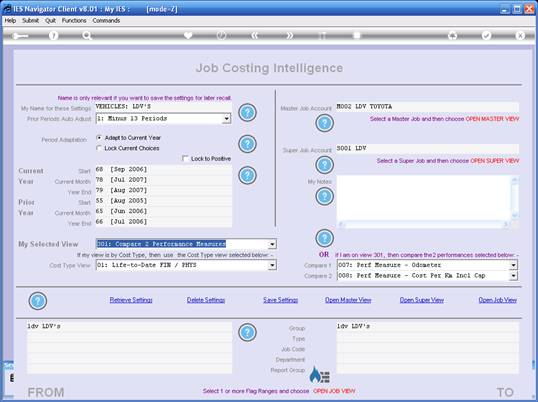

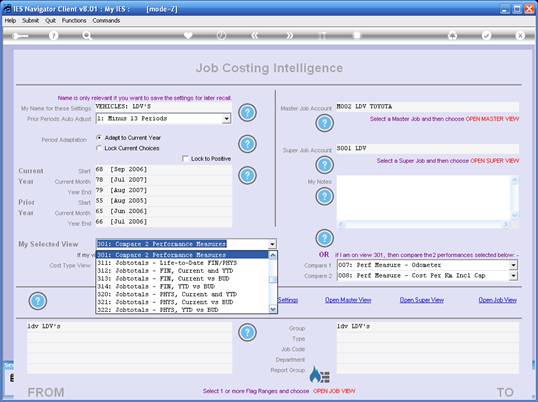

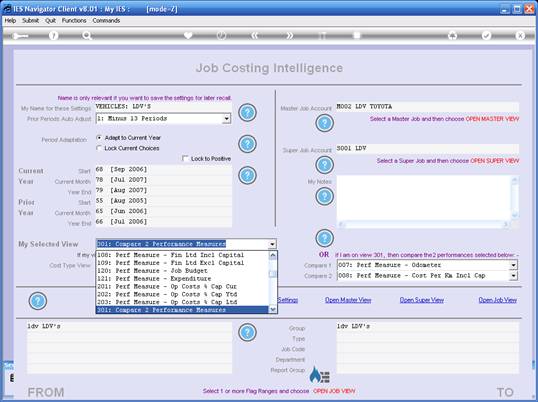

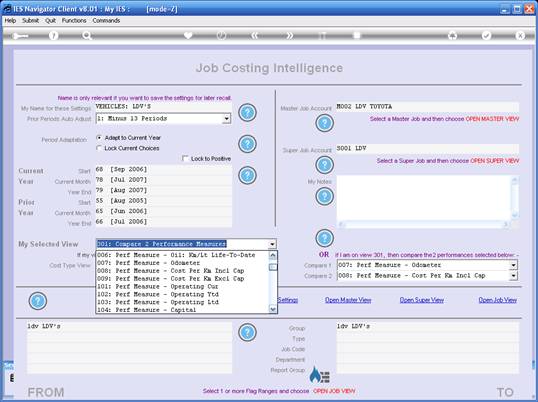

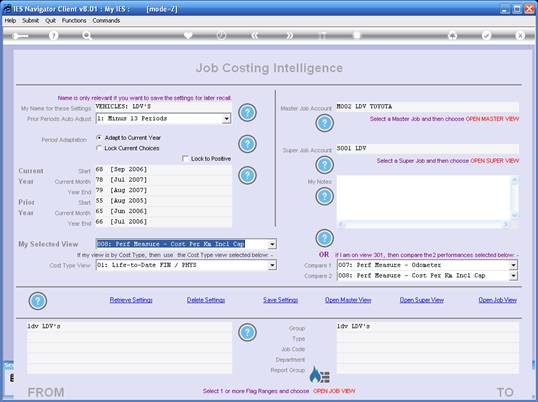

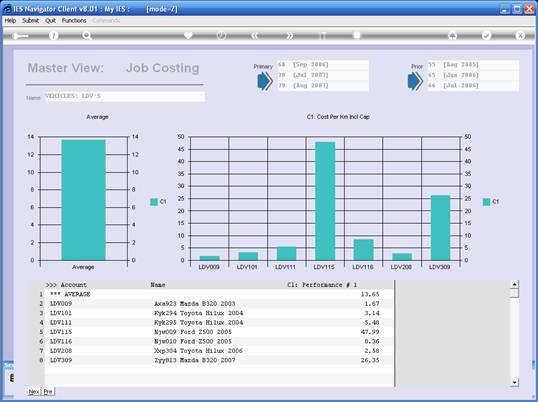

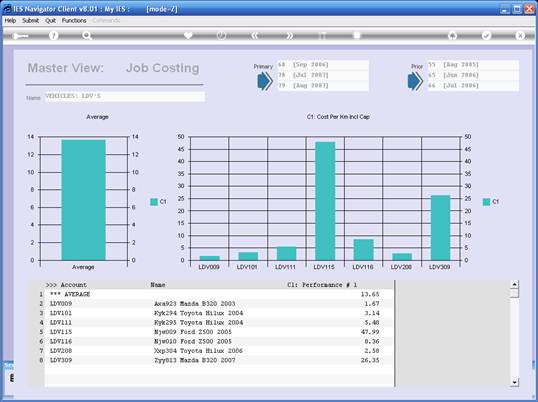

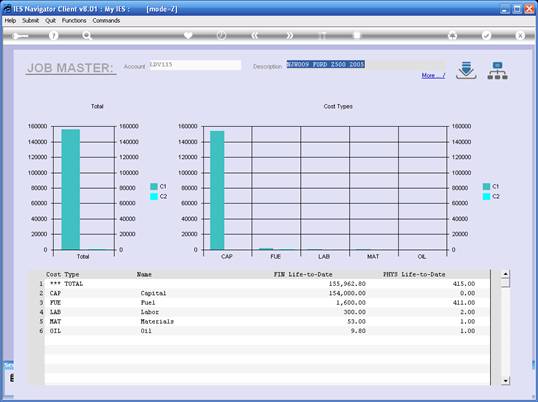

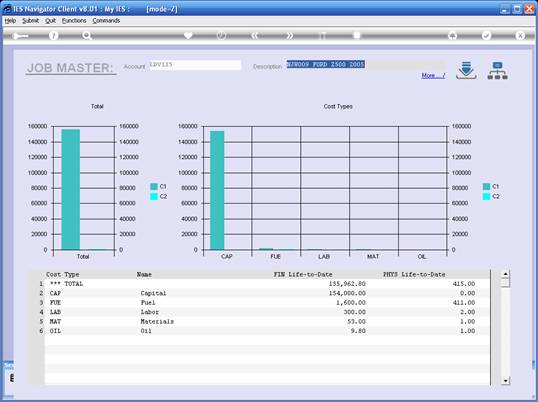

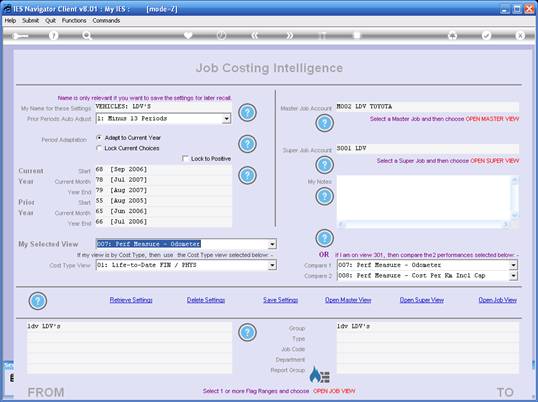

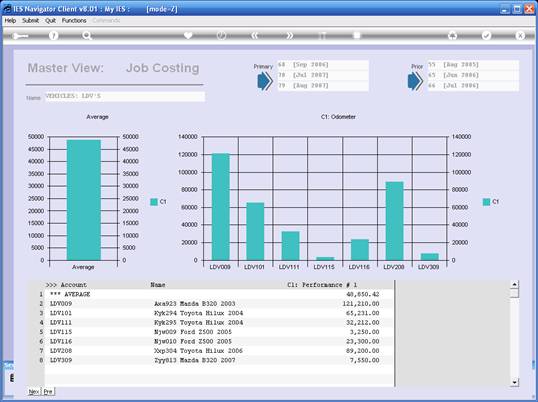

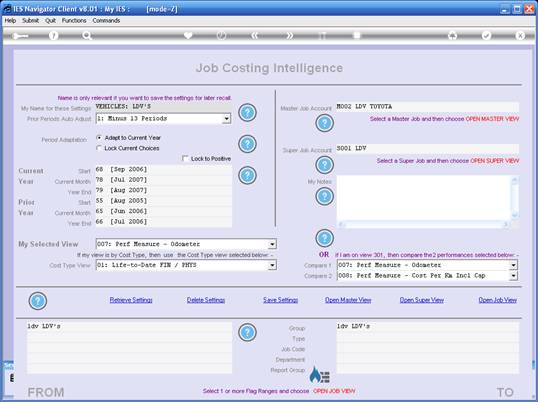

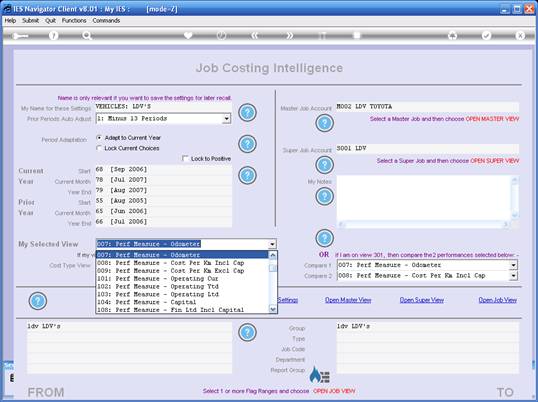

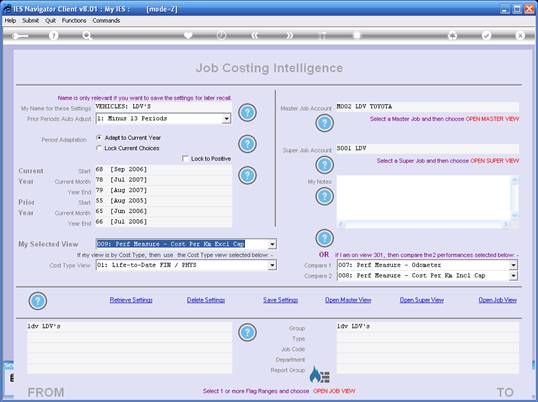

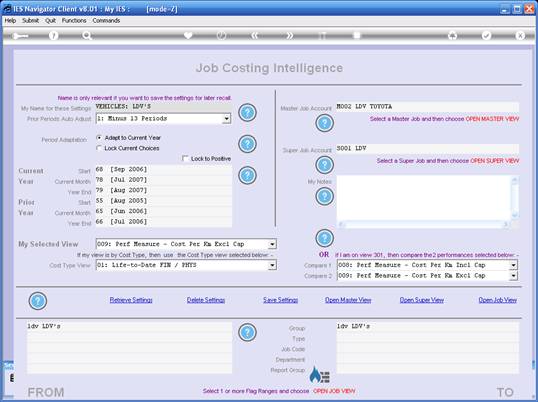

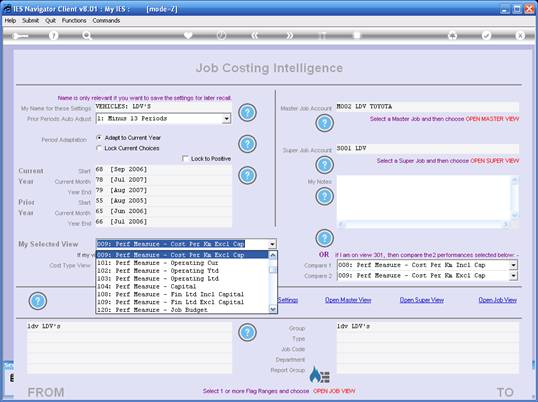

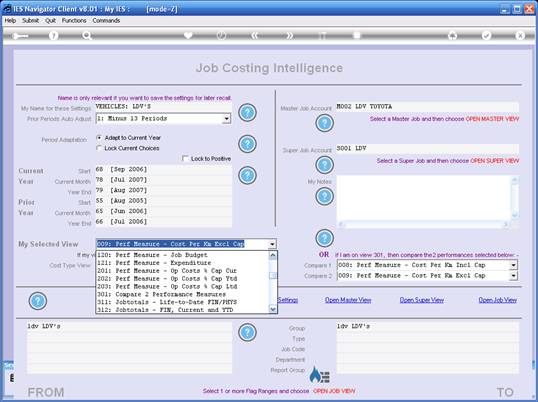

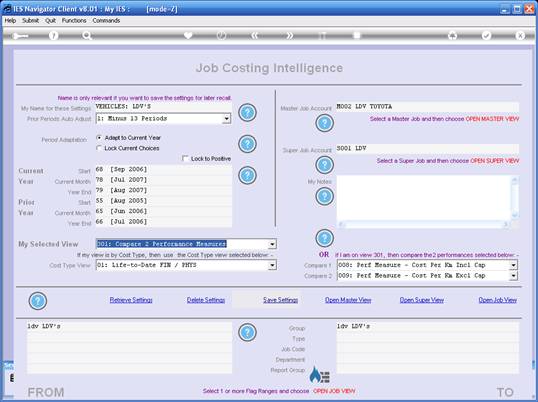

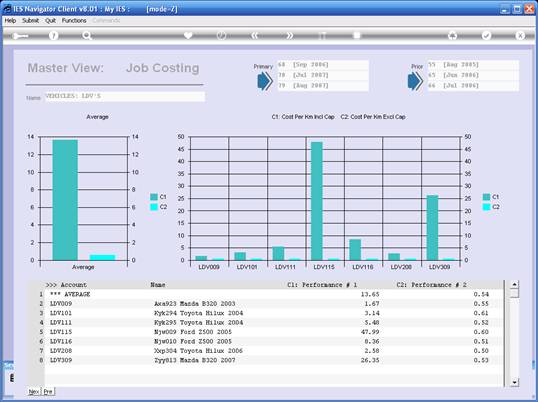

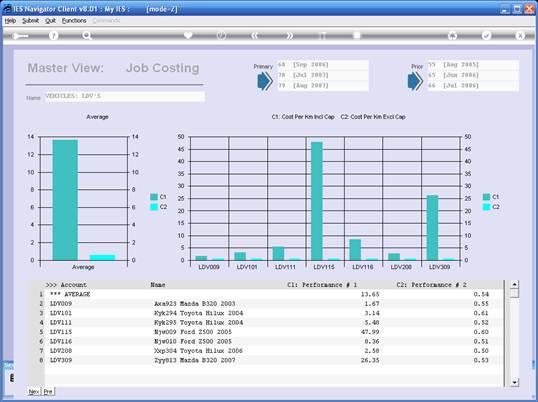

Slide notes: For Assets such as these, there

are Lifetime Operational Expenditure that are in addition to the Capital

Expenditure for the acquisition of the Assets. These Assets may break down,

may need servicing, may use fuel, may need refurbishing, etc. It is the Operational

Expenditure that we measure in the Job Costing system, and the Operational

Expenditure as a factor of the original Capital Amount is an important measurement

that can impact on any decision whether or not to replace an Asset.

|